Most people put off estate planning because they think it’s only for the wealthy or elderly. That’s simply not true-without a plan, your family faces unnecessary stress, delays, and costs when you’re gone.

At Family, Estate & Mediation Law, we’ve helped countless people create beginner estate planning guides tailored to their actual situation. This guide walks you through the documents you need, the mistakes to avoid, and the concrete steps to get started today.

Why Estate Planning Matters Right Now

Without an estate plan, your family faces real financial consequences. According to the National Council on Aging, roughly two-thirds of Americans lack any estate plan at all, leaving their families vulnerable to probate delays that can stretch 6 to 12 months or longer. During that time, assets sit frozen while courts process paperwork and creditors file claims. Your family cannot access funds for immediate needs-not for mortgage payments, not for medical bills, not for living expenses.

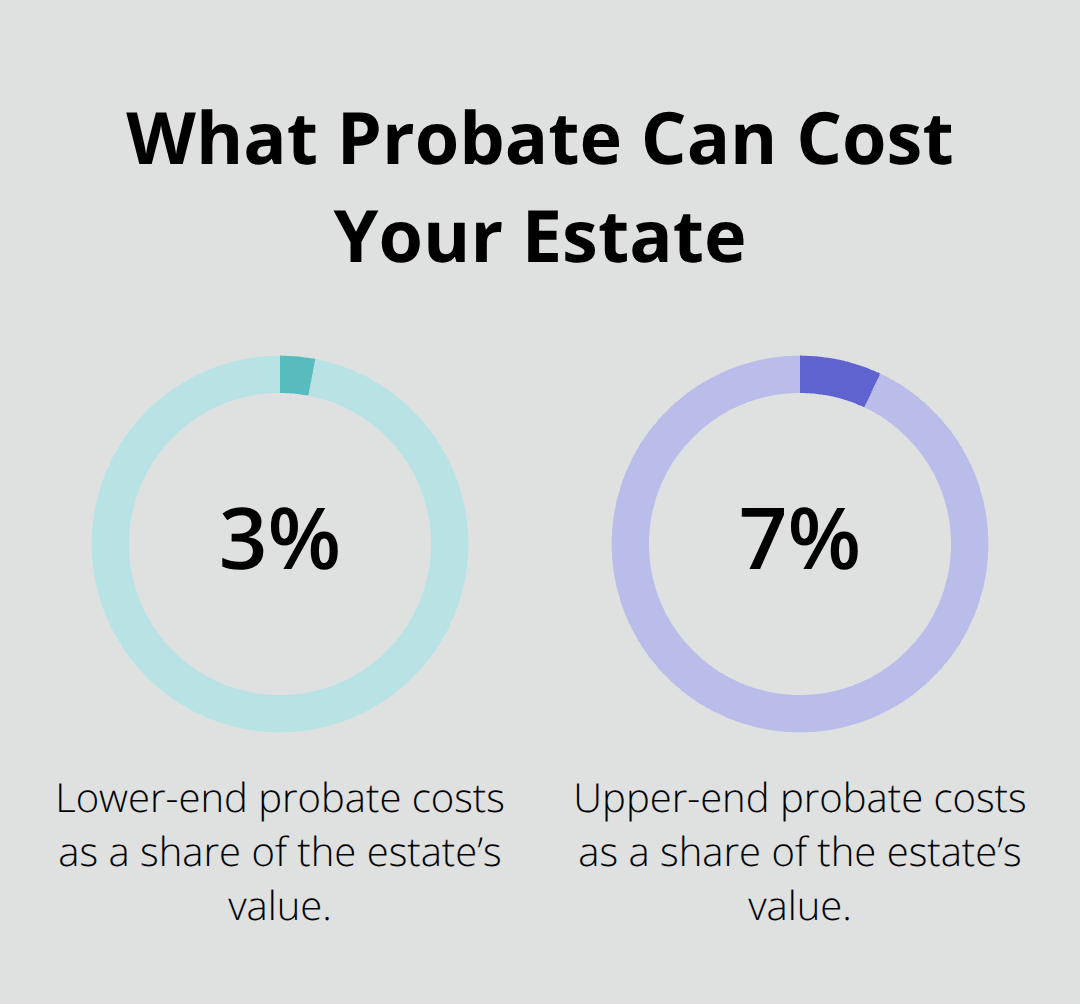

Probate costs also consume 3 to 7 percent of your estate’s total value in attorney fees, court costs, and administrative expenses, meaning a $500,000 estate could lose $15,000 to $35,000 to the probate process alone.

State Laws Make Decisions You Wouldn’t Make

Without clear instructions about who receives what, state intestacy laws step in and make those decisions for you-often contradicting what families actually want. If you have minor children and no named guardian in your will, a judge decides who raises them, not you. Estate planning puts you in control and protects what matters most.

Your Assets Reach Your Chosen Beneficiaries

When you create a will or trust, you specify exactly how assets transfer to your chosen beneficiaries. This matters because beneficiary designations on retirement accounts, life insurance policies, and payable-on-death accounts override whatever your will says. The National Council on Aging emphasizes that outdated beneficiary designations rank among the most common estate planning mistakes, often resulting in assets passing to ex-spouses or outdated beneficiaries instead of current family members.

A living trust lets you avoid probate entirely while maintaining privacy. Probate records become public documents, meaning anyone can see what your estate contained and who inherited it, but trust distributions remain confidential. For families with multiple properties or complex situations, a trust also creates a mechanism to manage assets if you become incapacitated, ensuring continuity without court involvement.

Tax Efficiency Starts Now, Not Later

The federal estate tax exemption currently sits at $13.99 million per person for 2025, but that threshold sunsets to approximately $7 million in 2026 unless Congress acts. Many states impose their own estate taxes with far lower exemptions, sometimes as low as $1 million. Even if your estate falls below federal thresholds today, strategic planning reduces what your heirs owe in taxes.

Annual gift exclusions allow you to give up to $19,000 per person tax-free in 2024, meaning a married couple can give $38,000 annually without triggering gift taxes. Lifetime gifting, irrevocable trusts, and charitable giving strategies work together to shrink your taxable estate during your lifetime rather than burdening your family after you’re gone. The documents you need to make this happen-and the mistakes that derail many families-require your attention next.

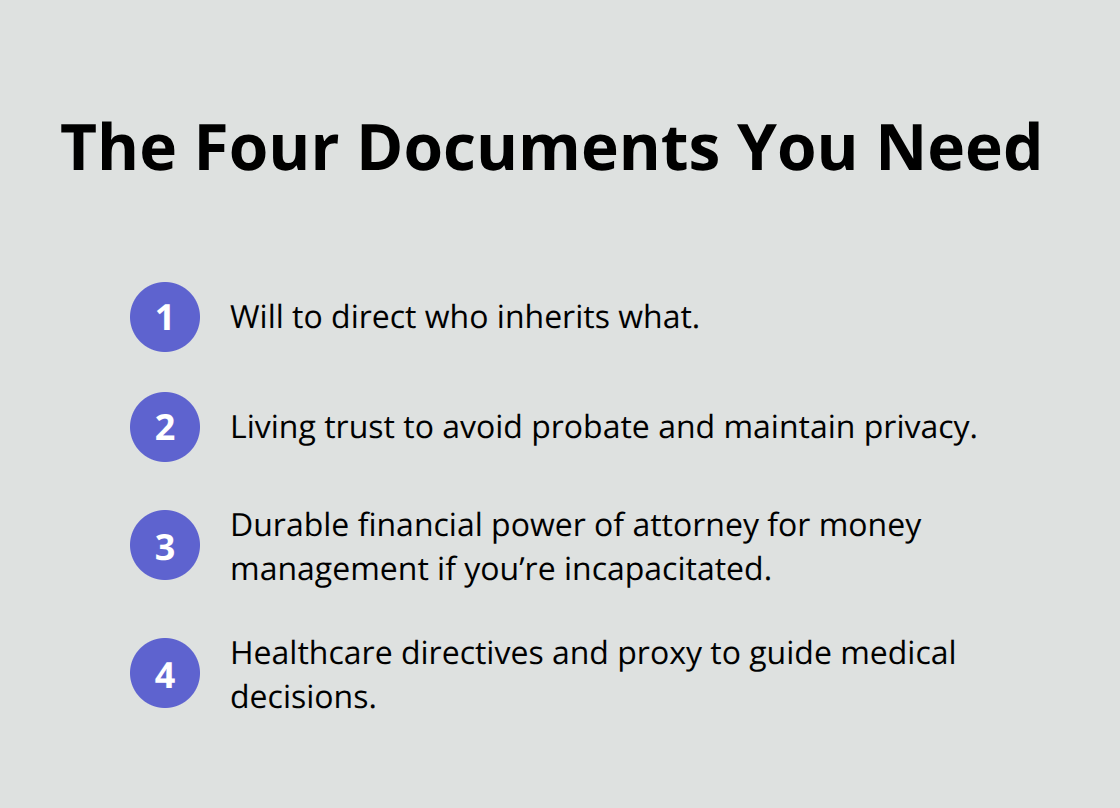

The Four Documents That Form Your Foundation

A will alone leaves your family scrambling. We at Family, Estate & Mediation Law see families struggle every month because they created a will but nothing else, then circumstances changed and nobody updated it. Your estate plan needs four working parts that function together: a will that directs asset distribution, a trust that bypasses probate, powers of attorney that cover financial decisions, and healthcare directives that guide medical care.

Wills and Trusts: Understanding the Difference

A will costs $300 to $1,000 to draft with an attorney, but it only addresses what happens after you die and must pass through probate. A living trust runs $1,000 to $5,000 depending on complexity, yet it avoids probate entirely, keeps your affairs private, and creates a mechanism for managing assets if you become incapacitated before death. According to the National Council on Aging, living trusts prove especially valuable for families with multiple properties or complex family dynamics because they prevent court involvement and maintain control without public disclosure.

The difference matters significantly. Probate proceedings become public record, so anyone can inspect what your estate contained and who inherited it, but trust distributions stay confidential. If you own real estate in multiple states, a trust becomes nearly mandatory since probate would occur in each state where you hold property, multiplying costs and delays.

Powers of Attorney: Handling Decisions While You’re Alive

Powers of attorney address the gap between now and death. A durable financial power of attorney names someone to handle your finances if you become unable to do so yourself, preventing the need for court-ordered guardianship. A healthcare power of attorney designates who makes medical decisions when you cannot, which matters far more than people realize since incapacity happens before death in many situations.

You can name different people for different roles-your spouse might manage finances while your adult child handles healthcare decisions. This flexibility allows you to match each person’s strengths to their specific responsibilities.

Healthcare Directives: Your Medical Preferences in Writing

An advance healthcare directive, sometimes called a living will, documents your preferences on life-prolonging treatments, artificial nutrition, pain management, and organ donation, then gives your healthcare proxy the authority to enforce those wishes. The National Council on Aging found that families without these documents face devastating disagreements during medical crises, with hospitals sometimes unable to proceed with treatment while relatives argue about what the incapacitated person would have wanted.

Store original documents in a safe deposit box or home safe, then provide your executor and agents with access details and secure login information. Discuss these roles in advance with whoever you name-many people accept the responsibility without understanding what it entails, then struggle when decisions arrive. Once you’ve identified the right people for these roles and drafted your documents, the next critical step involves ensuring your beneficiary designations align with your overall plan.

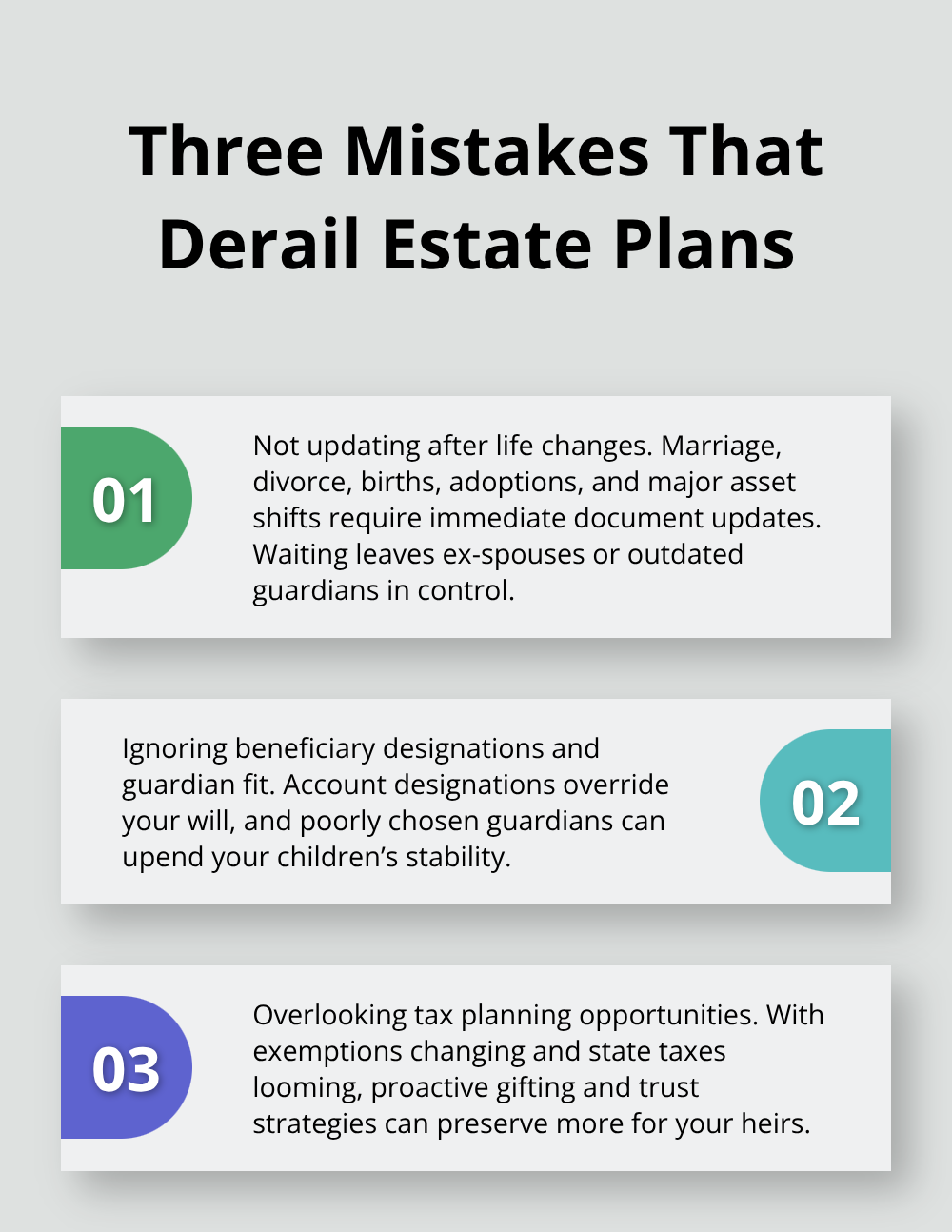

Three Mistakes That Derail Even Well-Intentioned Plans

Life Changes Demand Updated Documents

Life shifts, but most people’s estate plans remain frozen in time. Someone creates a will or trust, then marries, divorces, inherits money, has children, or experiences a significant financial shift-yet never updates a single document. The National Council on Aging reports that failing to update documents after major life changes ranks among the most damaging mistakes families make, often resulting in assets passing to ex-spouses, outdated guardians raising children, or beneficiaries who no longer exist.

A divorce should trigger immediate updates to remove a former spouse as executor, guardian, or beneficiary, yet many people assume the divorce decree handles this automatically. It does not. Your will still names them unless you file new documents. Marriage creates similar urgency: a new spouse may have no legal claim to your estate in many states if your will predates the marriage, meaning they could lose everything despite years together.

Major financial changes-inheriting a large sum, selling a business, acquiring rental properties-shift your tax situation dramatically, making old strategies obsolete or even harmful. We at Family, Estate & Mediation Law recommend reviewing your entire estate plan every three to five years minimum, and immediately after any marriage, divorce, birth, adoption, death in the family, significant asset acquisition, or retirement.

Beneficiary Designations and Guardian Choices Require Careful Attention

Outdated beneficiary designations on retirement accounts, life insurance policies, and payable-on-death accounts override your will completely, meaning an ex-spouse, deceased relative, or estate itself could receive assets you intended elsewhere. The National Council on Aging emphasizes that this single mistake causes more unintended distributions than any other planning error.

A woman who divorced but forgot to update her life insurance beneficiary designation watched her $250,000 policy pay directly to her ex-husband instead of her children. That money never touched her estate plan; it went straight to him because the designation superseded her will. Similarly, naming the wrong guardian for minor children-perhaps selecting someone based on family obligation rather than actual capability-creates real consequences.

A guardian must be willing to serve, geographically situated to provide stability, financially responsible, and aligned with your parenting values. Selecting a sibling out of obligation when your best friend is actually better equipped to raise your children leaves your kids with the wrong person for eighteen years.

Tax Planning Opportunities Protect Your Family’s Inheritance

Overlooking tax planning opportunities costs families thousands. The current federal estate tax exemption of $13.99 million per person in 2025 looks generous until you realize it sunsets to approximately $7 million in 2026, and many states impose taxes on much smaller estates.

Annual gifting of $19,000 per person ($38,000 for married couples) happens tax-free and reduces your taxable estate immediately. Irrevocable trusts, spousal lifetime access trusts, and charitable giving strategies exist specifically to minimize taxes, yet many people create simple wills that accomplish nothing on this front. A high-net-worth person with a $5 million estate who fails to implement any tax strategy could leave their heirs with $500,000 in unnecessary tax liability when straightforward planning prevents most of it.

Start Your Beginner Estate Planning Guide Today

List everything you own: real estate, bank accounts, retirement plans, life insurance, vehicles, business interests, and personal property with significant value. Include what you owe as well-mortgages, loans, credit card balances. This inventory takes an afternoon but gives your executor the complete picture they need to act quickly and accurately.

Identify the people who matter most to your plan: who manages your finances if you cannot, who makes healthcare decisions, who raises your minor children, and who inherits what. Be honest about each person’s capability and willingness to serve, since family obligation does not guarantee the right choice for handling complex financial decisions or raising your children. Your situation determines which documents you actually need-a young parent with modest assets needs different protection than a married couple with multiple properties or a high-net-worth individual exploring tax strategies.

We at Family, Estate & Mediation Law help individuals and families across Northeast Florida create plans tailored to their specific situation through professional estate planning guidance that ensures your documents comply with Florida law and accomplish what you intend. The documents you create now protect your family from months of probate delays, unnecessary taxes, and court decisions that contradict your wishes. Your family’s financial security and peace of mind depend on action, not intention.