Most Florida families put off estate planning because they think it’s complicated or unnecessary. The truth is simpler: without a plan, Florida’s intestacy laws decide who gets your assets, and courts make medical decisions for you.

We at Family, Estate & Mediation Law help Northeast Florida families build straightforward estate plans that actually work. This guide covers the Florida estate planning basics you need to protect what matters most.

Why Your Florida Estate Plan Matters Now

Florida’s lack of state income tax attracts retirees and families seeking financial advantages, yet this tax benefit creates a false sense of security about overall financial planning. Many Florida residents assume their assets will flow smoothly to loved ones without intervention, but state intestacy laws tell a different story. When you die without a will or trust in Florida, Statute 732.102 determines distribution based on a rigid formula: your spouse receives a portion, your children receive portions, and if you have no spouse or children, your parents, siblings, or distant relatives inherit instead. This outcome rarely matches what families actually want. Your ex-spouse might receive nothing while a sibling you haven’t spoken to in decades inherits a substantial share. Assets get tied up in probate for months or longer, costing thousands in court fees and attorney expenses that could have gone to your heirs.

Medical Decisions Without Your Input

The probate process handles asset distribution, but medical decisions present an even more urgent problem. Without a healthcare surrogate designation or living will, Florida courts appoint a guardian to make critical health decisions if you become incapacitated. This guardianship process is expensive, public, and slow-exactly what you don’t want during a medical crisis. A guardianship petition costs between $1,500 and $3,000 in filing fees and legal expenses before a judge even reviews your case. More importantly, the court decides who manages your medical care based on Florida Statute 744.331, not based on your personal preferences. A simple power of attorney designation costs far less and takes hours to complete, yet it gives someone you trust complete authority to make medical decisions aligned with your values. Without it, hospitals and courts make decisions for you.

Asset Titles and Beneficiary Designations Control Your Legacy

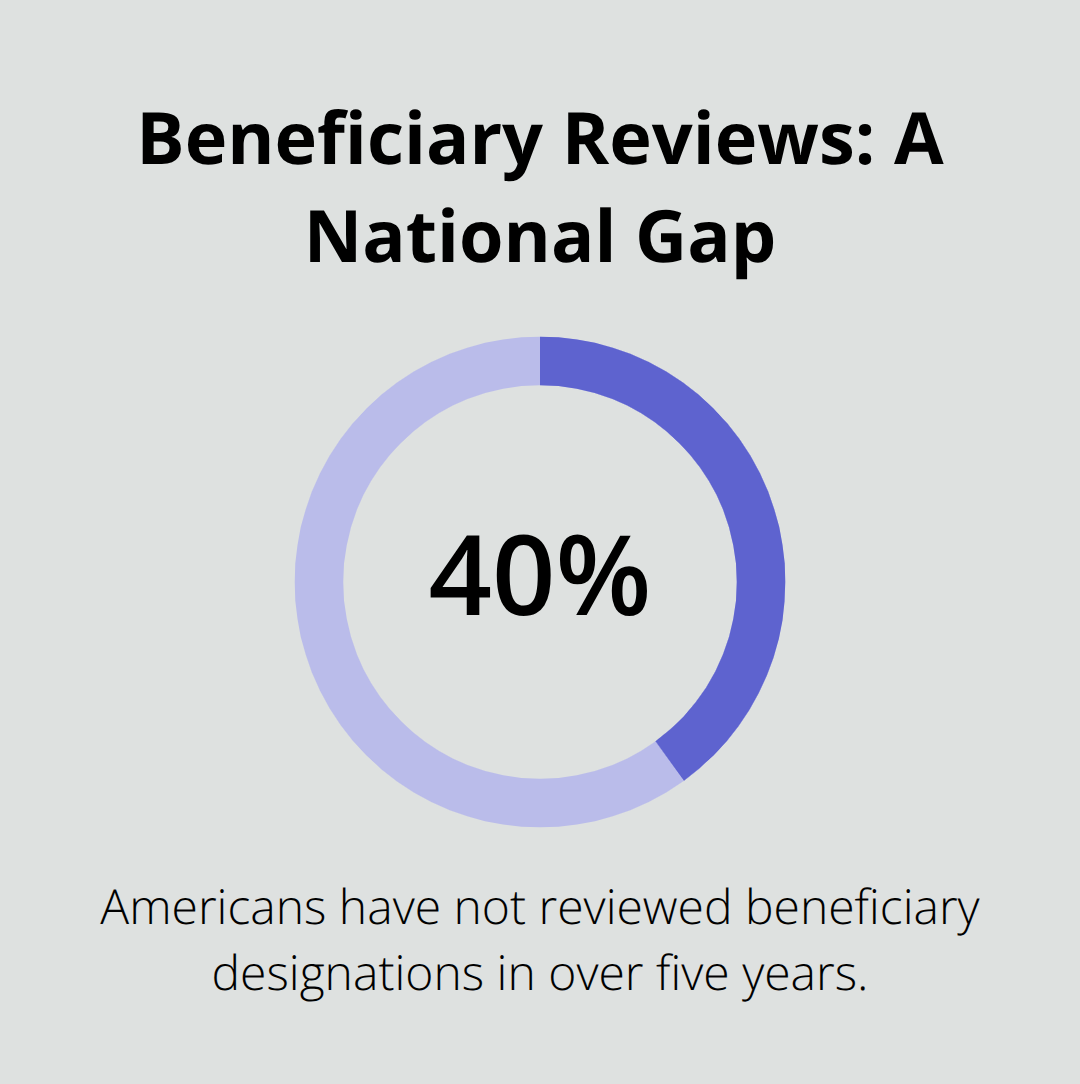

Many Florida families believe their will controls where assets go, but beneficiary designations on retirement accounts, life insurance policies, and transfer-on-death bank accounts override wills entirely. If your IRA names an ex-spouse as beneficiary and you never updated it after divorce, that ex-spouse receives the account regardless of what your will says. A 2023 survey by the Transamerica Center for Retirement Studies found that 40 percent of Americans have not reviewed their beneficiary designations in over five years.

The same applies to how you title your home. Property held as tenants by the entirety transfers automatically to your surviving spouse in Florida, bypassing probate for that asset. Property titled in your name alone goes through probate. A Ladybird deed, also called an enhanced life estate deed, transfers your home to named beneficiaries at death while you retain full control during life, avoiding probate entirely and preserving the stepped-up tax basis for your heirs (a significant tax advantage for your family). These technical details matter far more than most people realize-they determine whether your family pays thousands in probate costs or moves forward smoothly.

What Happens Next

The documents you need to put in place depend on your specific situation. Some families benefit from a simple will paired with a Ladybird deed, while others with multiple properties or blended families need a more comprehensive trust structure. The core documents every Florida family should consider form the foundation of any solid plan.

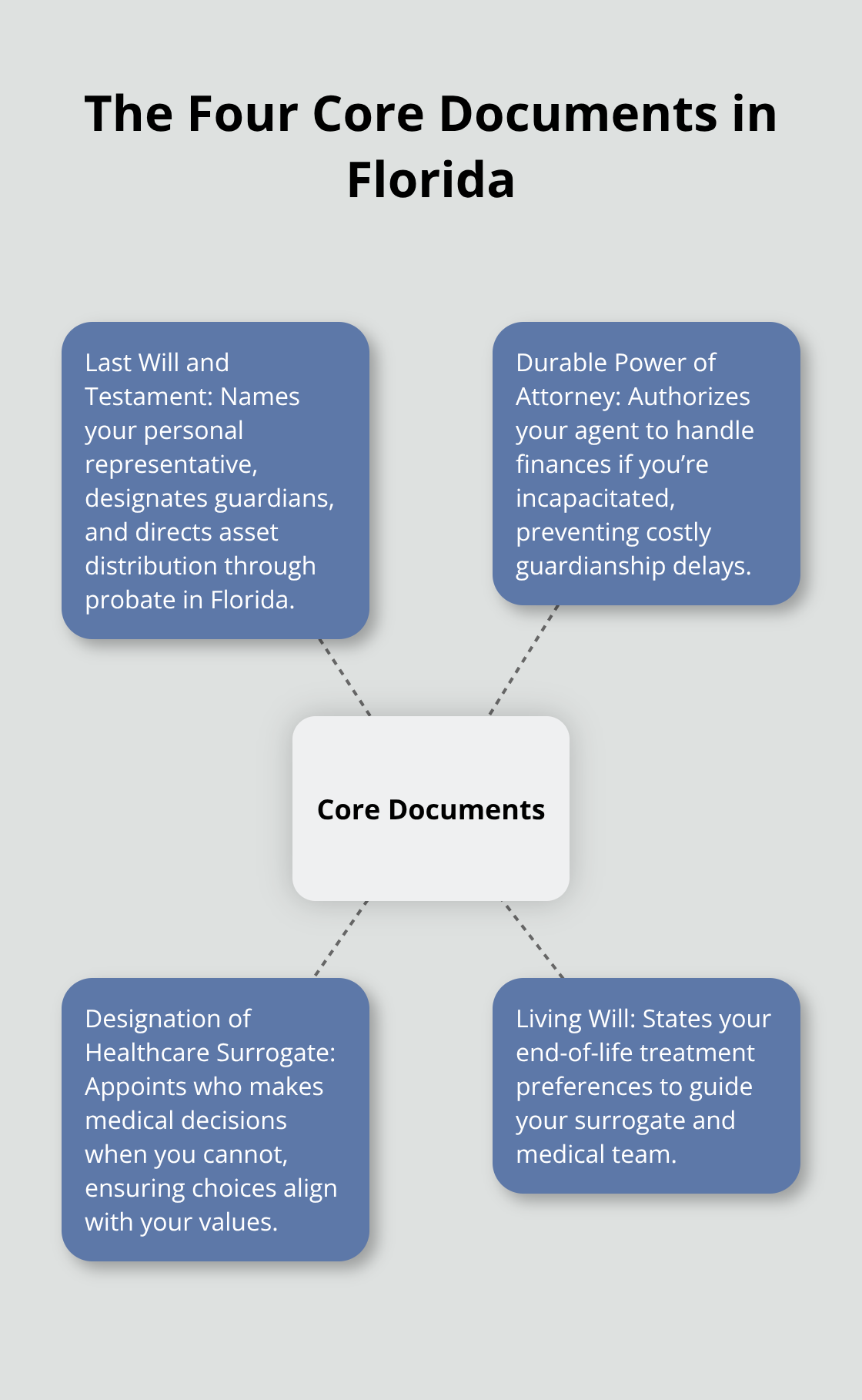

The Four Core Documents That Protect Your Florida Family

A will alone leaves your family vulnerable to probate delays and court costs that consume thousands of dollars your heirs could otherwise receive. Four core documents work together to handle asset distribution, medical decisions, and financial management. The first is a Last Will and Testament, which names your personal representative (executor) to manage probate, designates guardians for minor children, and directs how assets flow to beneficiaries. In Florida, your will must be signed in front of two witnesses and typically includes a self-proving affidavit to avoid probate delays caused by witness verification. Without naming guardians in your will, Florida courts decide who raises your children-a decision made by a judge who has never met your family.

Your Durable Power of Attorney Prevents Costly Guardianship

The second critical document is a Durable Power of Attorney for financial matters, which allows your designated agent to pay bills, manage investments, file taxes, and handle property transactions if you become incapacitated. This document prevents the need for expensive guardianship proceedings that cost between $1,500 and $3,000 in initial filing fees alone. Your agent acts immediately when you cannot, avoiding court delays that freeze your accounts and halt critical financial decisions during a health crisis.

Healthcare Decisions Require Two Documents Working Together

The third and fourth documents are a Designation of Healthcare Surrogate paired with a Living Will, which together let you specify who makes medical decisions and what end-of-life treatment you want if you cannot communicate your wishes. Without these documents, hospitals contact the court, triggering the guardianship process during a medical emergency when speed matters most. Your healthcare surrogate steps in immediately to direct your care according to your values, not a judge’s interpretation of Florida law.

When a Living Trust Becomes the Right Choice

Beyond these four foundational documents, a Living Trust makes sense when you own real property in multiple states, have a blended family, want to control how beneficiaries receive money over time, or simply want to avoid probate entirely. A Living Trust allows your successor trustee to distribute assets immediately after your death without court involvement, meaning your family accesses funds within weeks rather than months. The Ladybird deed (an enhanced life estate deed) works perfectly alongside a will for homeowners who want to avoid probate for their primary residence while keeping full control during life-you can still sell the home, refinance it, or change your mind and revoke the deed at any time.

Understanding Estate Planning Costs and Customization

Florida flat-fee pricing for estate planning typically ranges from $1,150 for an individual plan to $1,600 for a married couple, with Ladybird deed add-ons around $350, and these fees generally include consultation, drafting, revisions, and signing. The specific combination of documents your family needs depends on your assets, family structure, and goals. Your actual situation determines which documents matter most-a generic template cannot account for the details that protect your legacy and your family’s financial security.

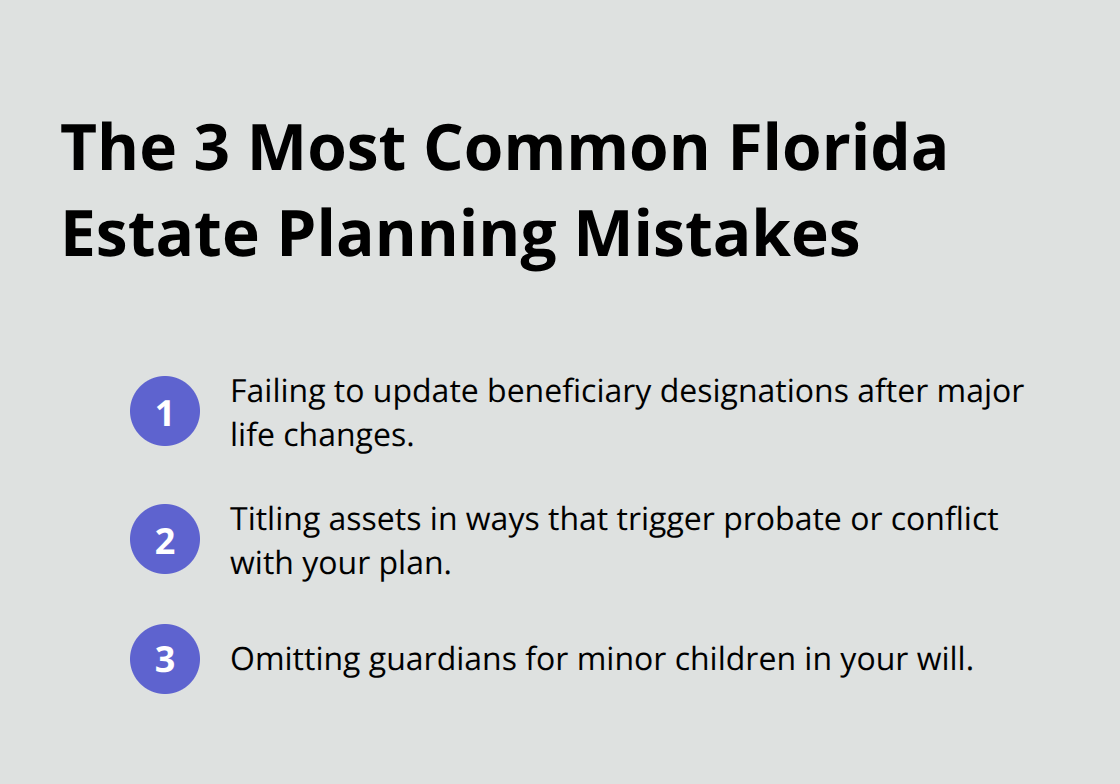

Common Estate Planning Mistakes Florida Families Make

Florida families make three critical mistakes that undo months of planning work, and the worst part is that these errors often go unnoticed until it’s too late to fix them. The first mistake happens after major life changes.

You get divorced, remarried, have a child, or experience a significant shift in your financial situation, yet your beneficiary designations stay frozen in time. The Transamerica Center for Retirement Studies found that 40 percent of Americans have not reviewed their beneficiary designations in over five years, and Florida families follow this pattern closely. Your IRA still names your ex-spouse as beneficiary. Your life insurance policy still lists your former partner. Your transfer-on-death bank account still flows to someone you no longer want to inherit. These designations override your will completely, meaning your current spouse and children receive nothing while your ex-spouse walks away with six figures.

Audit Your Beneficiaries After Life Changes

The solution is straightforward: audit every account that has a beneficiary designation within 30 days of any major life event. Call your bank, your employer’s benefits department, your insurance company, and your investment firm. Write down exactly who is named on each account. Update the beneficiaries immediately if they no longer match your current wishes. This single action prevents more inheritance disasters than any other estate planning step.

Title Your Assets to Match Your Estate Plan

The second mistake involves how you title your assets, which determines whether your family pays probate costs or avoids them entirely. Many Florida families title their home in their name alone, not realizing this triggers probate when they die. Others hold investment accounts in ways that conflict with their estate plan, or they fail to retitle assets after establishing a living trust. A Ladybird deed solves the home problem elegantly by transferring your residence to beneficiaries at death while you retain full control during life, avoiding probate and preserving the stepped-up tax basis your heirs need. If you own real property in multiple states or have a substantial investment portfolio, a living trust requires that you actually transfer assets into the trust during your lifetime. Many families create the trust document but never fund it, leaving assets outside the trust where they still go through probate.

Name Guardians Explicitly in Your Will

The third mistake is leaving your will without naming guardians for minor children. Florida courts appoint guardians based on what they think is best for the child, not based on your preferences. You might have a specific family member or close friend in mind to raise your children, but without naming that person in your will, a judge decides instead. This decision happens during probate when emotions run high and your family is grieving. Name your guardians explicitly in your will and discuss the responsibility with them beforehand to confirm they accept. These three mistakes are entirely preventable with action: review beneficiaries annually, ensure assets match your plan’s structure, and name guardians clearly in your will.

Final Thoughts

Your Florida estate planning basics protect your family from probate delays, court costs, and unwanted decisions made by judges who don’t know you. A will, durable power of attorney, healthcare surrogate designation, and living will form the foundation that controls your legacy instead of leaving it to state intestacy laws and court guardianship procedures. The specific documents you need depend on your assets, family structure, and goals, but waiting guarantees that Florida law will control your future instead of your choices.

Life changes constantly, and your estate plan must adapt with it. You marry, divorce, have children, experience health shifts, relocate, or watch your assets grow-each event demands a review of your documents to confirm they still reflect your current wishes. Review your plan every three to five years at minimum, and immediately after any major life event, because a beneficiary designation that made sense five years ago may now direct your retirement account to someone you no longer want to inherit.

We at Family, Estate & Mediation Law help Northeast Florida families in St. Augustine and Palatka build straightforward estate plans tailored to your specific situation. Contact us to schedule a consultation and take control of your family’s future today.