A financial power of attorney gives someone you trust the legal right to manage your money and property if you can’t do it yourself. Without one in place, your family could face serious complications during a medical crisis or when you’re unable to handle financial decisions.

At Family, Estate & Mediation Law, we see firsthand how the right financial power of attorney protects families from costly delays and disputes. This guide walks you through the decisions you need to make before signing.

What a Financial Power of Attorney Actually Does

Your Agent’s Financial Authority

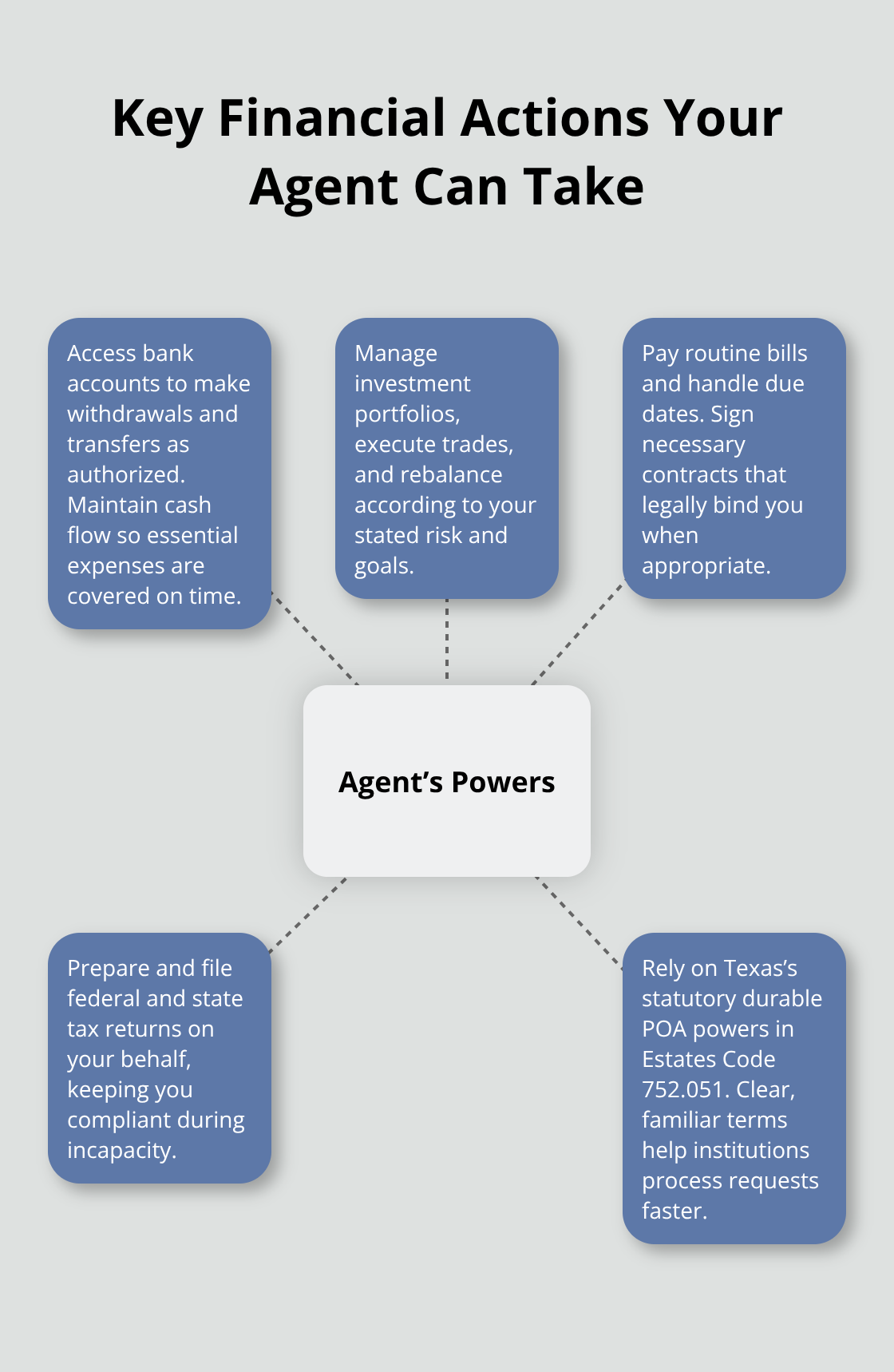

A financial power of attorney hands your agent access to specific financial tools and accounts. This isn’t a vague grant of authority-it’s a detailed permission slip for concrete actions. Your agent can withdraw money from your bank accounts, manage investment portfolios, pay bills from your checking account, file tax returns on your behalf, and sign contracts that bind you legally. In Texas, the statutory durable power of attorney form provided under Texas Estates Code 752.051 outlines these powers clearly, though many people skip reading it carefully before signing.

Scope Matters More Than You Think

The scope of authority determines everything. A general durable POA grants broad authority across all financial matters, while a limited POA restricts your agent to specific tasks like selling a particular property or managing only investment accounts. We at Family, Estate & Mediation Law strongly recommend choosing limited authority unless you genuinely need your agent to handle everything. Too many people hand over unrestricted power out of convenience, then regret it when they realize their agent can gift away assets, redesignate beneficiaries on retirement accounts, or retitle property without additional approval.

Your agent’s authority becomes your liability. If they misuse it, you’re responsible for their actions, which is why trustworthiness and competence matter far more than family ties.

Real Estate Transactions Require Extra Steps

Real estate transactions deserve special attention because they require additional formalities. If your POA includes real estate authority in Texas, the document must include a precise legal description of the property and be recorded in the county deed records where the property sits. Banks and financial institutions have statutory grounds to reject a POA under Texas Estates Code 751.206, and they do-eleven reasons exist, including doubt about validity or concerns the agent is acting beyond scope.

This happens frequently enough that you should keep multiple certified copies on hand and inform your financial institutions in advance that you’ve created a POA.

Professional Fiduciaries as an Alternative

Professional fiduciaries (bonded and insured trust companies or attorneys) offer an alternative if you can’t find a trustworthy family member or friend. They cost more, typically charging annual fees or hourly rates, but they uphold fiduciary duties without personal conflicts and understand the technical requirements institutions demand. Whether you choose a family member or professional, name a successor agent in your POA so that if your primary agent dies, becomes incapacitated, or refuses to serve, authority transfers smoothly without court involvement.

The decisions you make about agent selection and scope of authority directly shape how well your financial plan protects you during a crisis-and how much risk you actually take on.

When You Should Create a Financial Power of Attorney

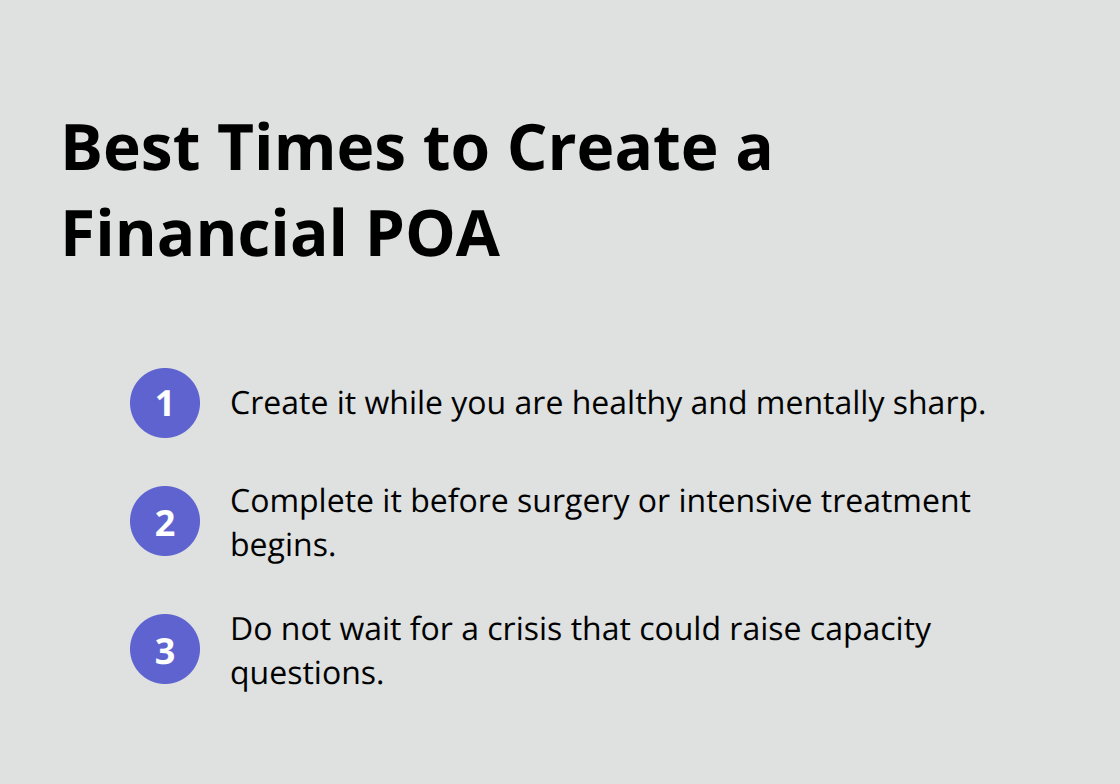

Timing matters more than most people realize. You should create a financial power of attorney while you’re healthy and mentally sharp enough to make clear decisions about who handles your money. Many families wait until a crisis hits-a stroke, a car accident, a cancer diagnosis-then scramble to find an attorney who can draft documents quickly. At that point, questions arise about whether you had the mental capacity to create a valid POA, which can invalidate the entire document and force your family into expensive guardianship proceedings. The moment to create your POA is now, not when you’re in a hospital bed.

Long-Term Care and Aging

Parents in their sixties and seventies often postpone this conversation because they feel healthy. Then one parent develops early-stage dementia or needs assisted living, and the other parent realizes they can’t access joint accounts, pay property taxes, or make investment decisions without a POA already in place. Without one, siblings may disagree about financial choices, banks may freeze accounts pending court orders, and care decisions get delayed while legal paperwork catches up. If you have aging parents, start the conversation now. Ask them directly whether they have a financial POA naming you or another trusted person. If they don’t, offer to help them schedule an appointment with an attorney. Texas law requires a notary present when signing a financial POA, and if real estate is involved, the document must be filed with the county clerk-these aren’t obstacles, just practical steps that take a few hours to complete.

Serious Health Conditions and Recovery

A diagnosis of cancer, heart disease, or any condition requiring surgery or extended treatment creates an immediate need for a financial POA. Even if you expect to recover fully, surgery and anesthesia can temporarily impair your judgment, and recovery periods often last longer than expected. Medical bills arrive, insurance claims need processing, and mortgage payments don’t pause while you heal. If you’re married, your spouse can usually access joint accounts, but if you’re single, divorced, or your spouse lacks financial knowledge, an agent with clear authority prevents delays. In Texas, a durable power of attorney continues operating even if you become incapacitated, which means your agent can handle finances without waiting for a doctor to declare you incompetent or for a court to appoint a guardian.

Military Service and Prolonged Absences

Active-duty military personnel and their families face unique timing pressures. Deployments last months or years, and managing finances remotely becomes complicated when you can’t appear in person to sign documents, verify identity, or handle time-sensitive transactions. A durable power of attorney executed before deployment lets your spouse, parent, or trusted friend manage bills, handle insurance claims, and make investment decisions without waiting for your return. This prevents the situation where a mortgage payment gets missed because nobody had authority to access the account, or a tax return doesn’t get filed because only you knew the details. Once you’ve identified the right time to create your POA and understand what triggers that need, the next critical decision involves selecting the right person to act as your agent-a choice that determines whether your financial interests stay protected or face serious risk.

Common Mistakes People Make With Financial Powers of Attorney

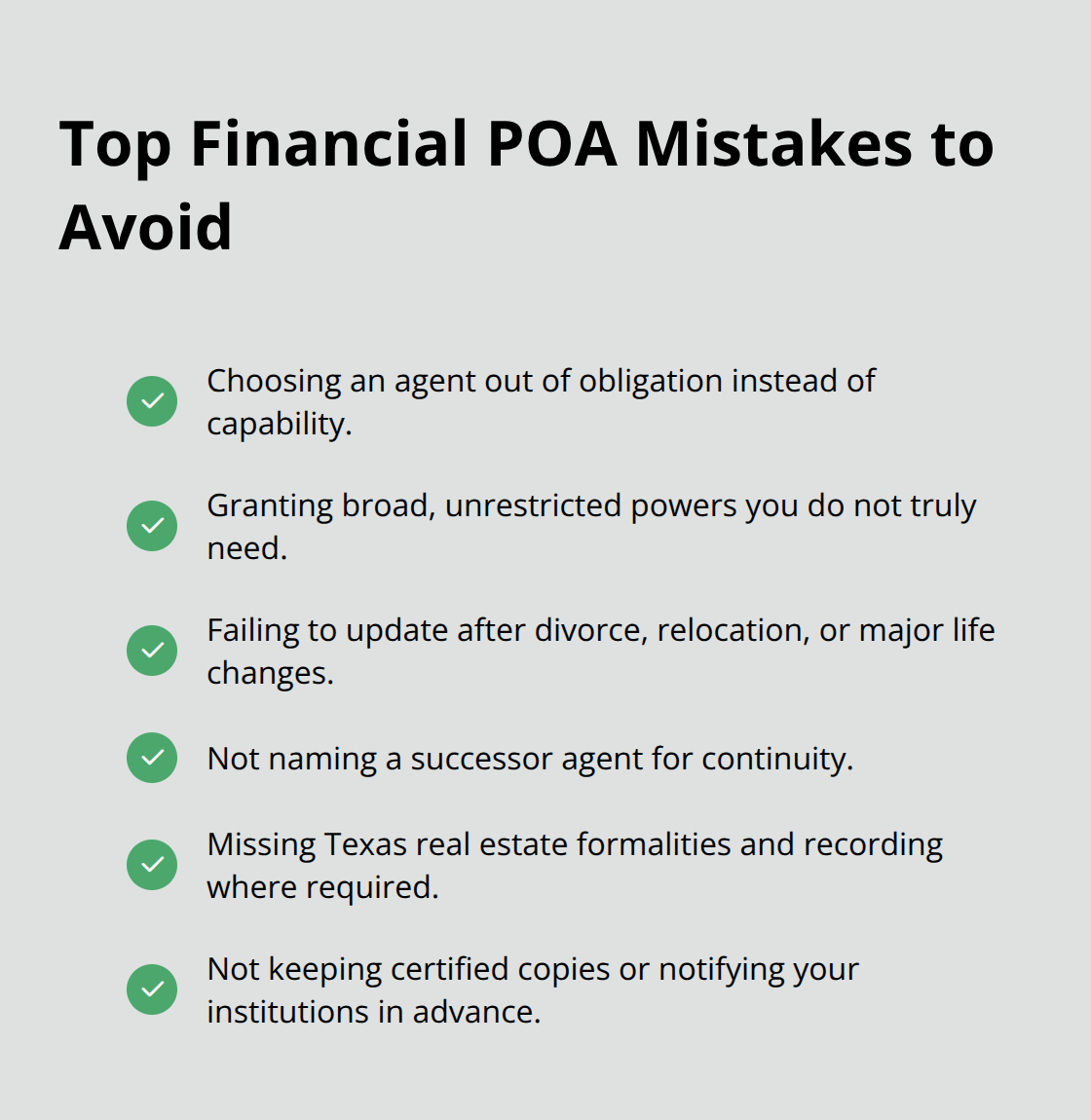

The most damaging mistakes happen before you ever sign the document. Families struggle with POAs that were created carelessly, and most problems trace back to three preventable errors. First, people appoint the wrong agent because they choose based on family obligation rather than actual capability. Your sibling might be your closest relative, but if they struggle with money management, ignore emails, or live three states away, they will mishandle your finances when you need them most. Trustworthiness and competence matter infinitely more than blood relation.

Second, people fail to limit their agent’s authority, handing over unrestricted power when they could have specified exactly which accounts, assets, or decisions the agent can touch. This creates unnecessary risk because your agent can then gift away assets, redesignate beneficiaries on retirement accounts, or make investment changes you’d never approve. Third, people create a POA once and forget about it, never updating the document after divorce, relocation, job loss, or major changes in family circumstances. A POA naming your ex-spouse as agent after you’ve divorced might still be valid depending on your state’s laws, but it creates conflict and opens doors to challenges from other family members.

Select an Agent Who Will Show Up When You Need Them

The agent you name today must be someone who will actually appear when a financial crisis hits. This means choosing someone organized enough to handle paperwork, responsive enough to answer calls from banks and doctors, and geographically close enough to access physical documents and sign papers in person when needed. If your primary agent lives across the country and works sixty-hour weeks, they will struggle to pay your bills on time or manage a real estate transaction requiring notarized signatures. Name a successor agent in your POA so authority transfers smoothly if your first choice dies, becomes incapacitated, or simply refuses to serve when the time comes. Many people skip this step, assuming it won’t matter, then their family ends up in court fighting over guardianship when the primary agent cannot help. Professional fiduciaries offer an alternative if family members aren’t reliable. They charge fees, but they provide continuity, understand institutional requirements, and hold bonded insurance protecting against their own misconduct. Whatever path you choose, have a detailed conversation with your agent about what decisions they will face, your financial values, and exactly how you want them to handle situations involving large gifts, investment changes, or medical-related expenses.

Restrict Powers to Prevent Misuse Before It Starts

A limited POA that restricts your agent to specific financial tasks reduces risk far more effectively than hoping you chose someone trustworthy. Instead of granting broad authority over all accounts, specify which bank accounts your agent can access, whether they can gift money to themselves or family members, whether they can change beneficiaries on retirement accounts, and whether they can refinance your home. This specificity prevents the scenario where an agent co-mingles your funds with theirs, makes unauthorized purchases, or drains accounts to pay for their own problems. Banks and financial institutions already reject POAs regularly under statutory grounds, so adding clear limitations actually helps institutions accept your document faster because they understand exactly what authority you’ve granted. If your agent needs to handle real estate in Texas, include the precise legal description of the property and file the POA with the county clerk where the property sits. This extra step prevents disputes about whether your agent can actually sell or refinance that specific property.

Update Your POA After Major Life Changes

Life changes demand POA updates. A divorce should trigger an immediate review of your POA because your ex-spouse may retain authority depending on your state’s laws, creating conflict and vulnerability. A relocation to a different state might affect which POA form you need and how institutions recognize your document. A significant change in your financial situation (inheritance, business sale, major debt) requires you to reconsider whether your agent’s current authority still matches your actual needs. Job loss, health decline, or family conflict can also signal that your chosen agent no longer fits the role. Many people assume a POA lasts forever without modification, but that assumption costs families thousands in legal fees and court battles when outdated documents create confusion. Schedule a review with an attorney every three to five years, or immediately after any major life event, to confirm your POA still reflects your wishes and your agent remains the right choice.

Final Thoughts

A financial power of attorney protects your family from financial chaos when you face a health crisis or unexpected incapacity. The decisions you make today about who holds your authority and what limits you place on that authority will determine whether your family manages finances smoothly or struggles through court intervention. Before you sign, confirm that your chosen agent understands the responsibility, that the scope of their authority matches your actual needs, and that you’ve named a successor in case your first choice cannot serve.

Your financial power of attorney works alongside other planning documents like your will and healthcare directive to create a complete picture of how you want your life and finances managed. Without one, your family may need court intervention through guardianship or conservatorship, which costs thousands of dollars and takes months to complete. With one in place, your agent can pay bills, manage investments, handle real estate transactions, and file taxes without waiting for judicial approval.

Contact us at femlg.com to discuss your financial power of attorney and ensure your family receives the protection it needs. We help families across Northeast Florida create documents that reflect their values and their trust in the person they’ve chosen to act as agent.