A power of attorney is one of the most important documents you’ll ever sign, yet many people rush through it without thinking clearly about what they’re granting away. At Family, Estate & Mediation Law, we see clients make costly mistakes because they didn’t consider the full scope of POA planning considerations before handing over authority.

The right preparation now prevents serious problems later. This guide walks you through the essential factors that make the difference between a smooth grant and a legal headache.

What a Power of Attorney Actually Does

The Legal Foundation and How It Works

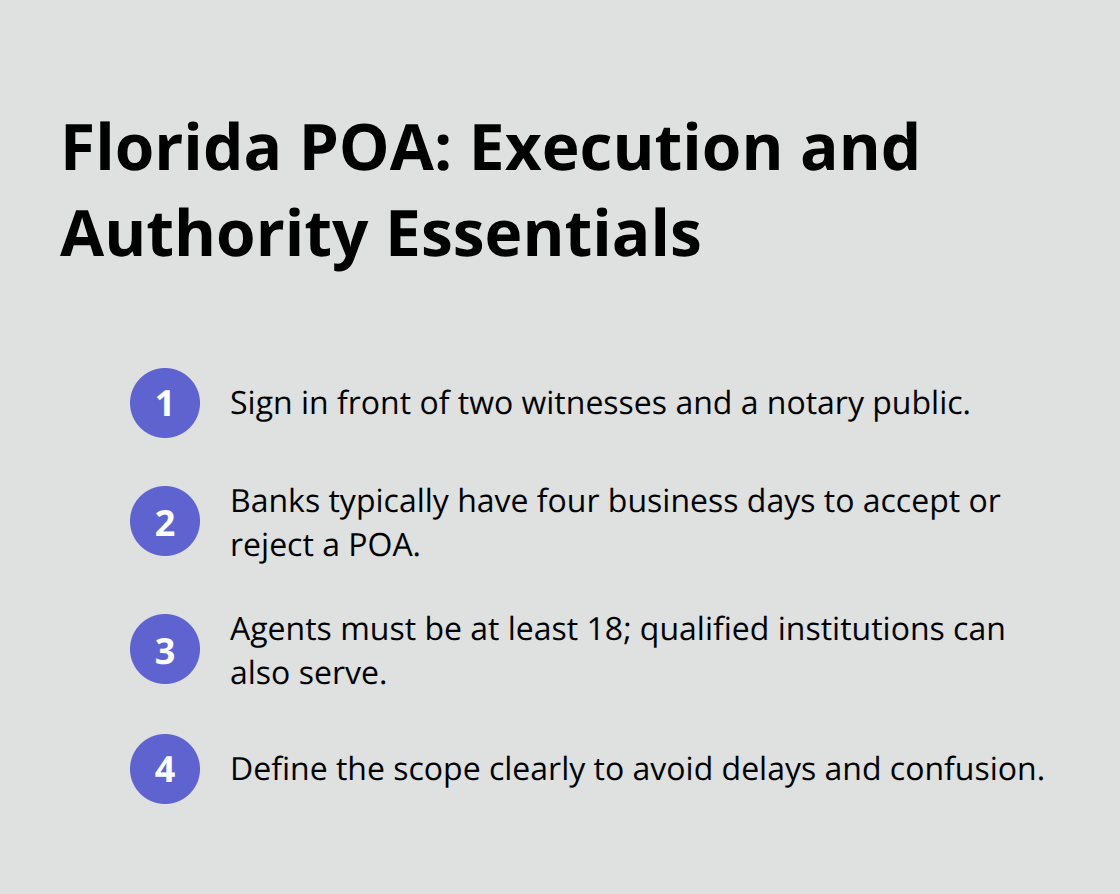

A power of attorney is a legal document that authorizes someone you trust to act on your behalf in financial and legal matters. In Florida, Chapter 709 of the Florida Statutes governs this document and expanded the POA framework significantly in 2011 to give financial institutions and third parties clearer rules about accepting these documents. The person you appoint, called your agent or attorney-in-fact, can handle banking, investments, real estate transactions, and other financial decisions if you become unable to manage them yourself. A durable POA remains effective even if you become incapacitated, which is why nearly all modern POAs include explicit durability language stating the authority continues despite your incapacity. A non-durable POA, by contrast, terminates immediately if you lose mental capacity, making it far less practical for most people.

Florida law requires your POA to be signed in front of two witnesses and a notary public to be valid, and financial institutions typically have four business days to accept or reject it. Your agent must be at least 18 years old and a natural person, though financial institutions with trust powers can also serve as agents. The scope of authority you grant determines what your agent can and cannot do-you might limit them to paying bills only, or grant broad authority over all financial matters. Specific language about which powers you grant prevents friction with banks and investment firms that want clarity before accepting your document.

Durable vs. Non-Durable POAs

The distinction between durable and non-durable powers of attorney matters significantly for your planning. A durable POA survives your incapacity and continues to protect your interests when you need it most. Non-durable POAs lose all force the moment you lack mental capacity, which defeats the purpose for most people who sign these documents to prepare for potential incapacity. Florida recognizes out-of-state POAs if they met the other state’s requirements at execution, but Florida residents should use Florida-compliant documents to minimize delays and reduce the likelihood that third parties will request costly counsel opinions to verify validity.

What a POA Does Not Cover

Many people confuse a POA with other documents, believing it gives someone authority to make medical decisions or that it automatically creates a guardianship. Your POA handles only financial and legal matters; healthcare decisions require a separate health care proxy or surrogate designation under Florida Chapter 765. A POA also does not replace a will or bypass probate-it functions purely as a tool for managing your affairs while you’re alive. Some clients mistakenly think they need a court-ordered guardianship to handle finances for an aging parent, when a properly drafted POA would accomplish the same goal without court involvement and at a fraction of the cost.

Retaining Control and Revoking Authority

Signing a POA does not mean losing control of your finances and property. You retain full authority and can revoke the document at any time as long as you remain mentally capable. You can also name successor agents to step in if your first choice becomes unable or unwilling to serve, providing continuity without court intervention. The POA takes effect when you sign it, and you should notify your agent and any institutions relying on the document if you revoke it to prevent continued use after revocation.

Moving Forward With Confidence

Understanding what a POA actually does-and what it does not-sets the foundation for smart planning decisions. The next step involves selecting the right person to act as your agent, since this choice determines whether your POA works smoothly or creates complications down the road.

Who Should You Choose as Your Agent

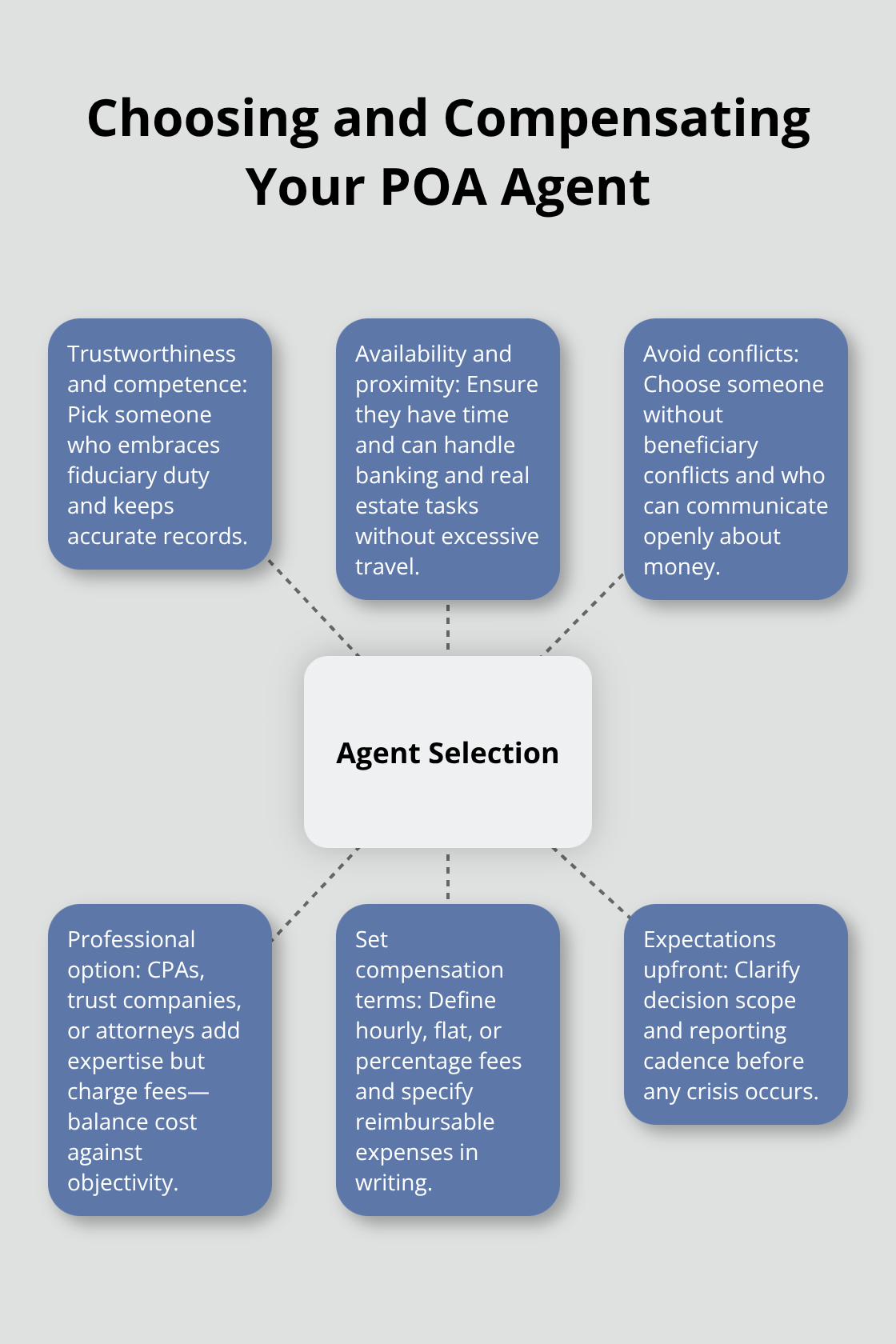

Selecting your agent is the single most consequential decision in POA planning because this person will have direct access to your bank accounts, investment portfolios, and property. The wrong choice leads to financial loss, delayed transactions, or family conflict that lasts years. We at Family, Estate & Mediation Law have observed clients appoint agents who lacked the organizational skills to maintain records, who faced creditor claims against the principal’s accounts due to their own financial problems, or who simply disappeared when the POA needed activation. Your agent must demonstrate trustworthiness, competence, and willingness to accept the fiduciary responsibility that comes with the role.

Identifying the Right Candidate

The best agent demonstrates financial responsibility in their own life, has the time to manage your affairs properly, and lives close enough to handle banking and real estate matters without excessive travel. If you choose a family member, that person should have no conflicts of interest with other beneficiaries and should feel comfortable discussing money openly with you before any crisis occurs. Professional agents-such as trust companies, certified public accountants licensed in Florida, or elder law attorneys-bring objectivity and expertise but charge fees that reduce your estate. Florida law defines qualified agents eligible for reasonable compensation as including your spouse, direct heirs, Florida-licensed lawyers or CPAs, trust companies, and Florida residents who serve as agents for no more than three principals simultaneously.

When you name a professional, clarify in writing whether they receive hourly fees, flat fees, or a percentage of assets managed, and confirm they understand your specific financial situation and goals. Family agents often serve without compensation, but you can authorize reimbursement for documented expenses like safe deposit box fees, travel costs, or professional consultation fees they incur while managing your affairs.

Avoiding Agents Who Cannot Perform

Florida law requires your agent to be at least 18 years old and mentally capable of handling financial decisions. You cannot appoint someone with active substance abuse issues, untreated mental illness, or a history of financial mismanagement, because the agent’s incompetence becomes your problem when banks reject transactions or your agent fails to pay bills on time. Do not appoint multiple agents to act jointly unless you are absolutely certain they can cooperate, because unanimous agreement requirements slow everything down during emergencies.

If you name co-agents with no specification about how they act, Florida law allows each to act independently, which means one agent could make decisions that conflict with the other’s intentions. Specify in your POA whether co-agents must agree unanimously, act by majority, or can act individually so there is no ambiguity when your agents need to move quickly.

Preparing Your Agent for Success

Once you choose your agent, sit down with them before you sign the POA and explain exactly what you expect. Walk through your financial accounts, investment holdings, real estate, and any business interests so they understand the scope of what they will manage. Give them a copy of the signed POA, your banking passwords and account numbers, locations of important documents, and contact information for your accountant, investment advisor, and attorney.

Create a written summary of your financial goals (whether you want the agent to preserve capital, generate income, or pay down debt) because agents who lack this guidance may make decisions that contradict your values. Tell your agent whether they should maintain detailed records of every transaction or simply provide annual accountings. Discuss whether they can hire professionals to help, because a competent agent knows when to bring in a CPA or attorney rather than attempting complex tax returns or real estate closings without expertise. This preparation transforms your agent from someone who merely holds a document into someone who actively protects your interests and understands your vision for your financial future.

Critical Planning Steps Before Granting POA

Create a Complete Financial Inventory

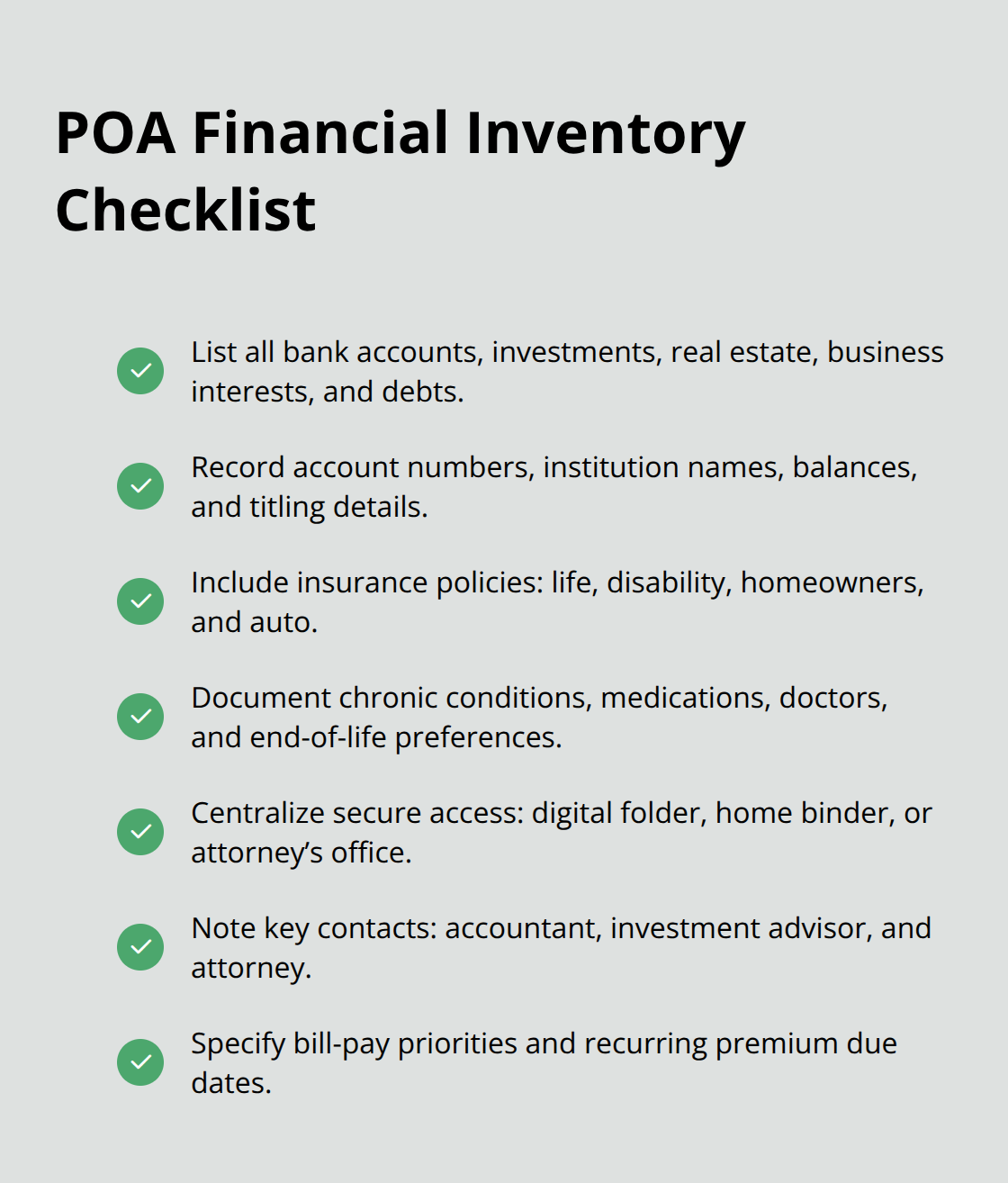

Before you hand over financial authority to anyone, you need a complete picture of what you own, what you owe, and what decisions matter most to your family. Most people skip this step and regret it when their agent discovers hidden accounts, conflicting instructions in other documents, or tax complications nobody anticipated. Create a financial inventory that lists every bank account, investment portfolio, real estate property, business interest, and outstanding debt. Include account numbers, institution names, approximate balances, and the names on title so your agent knows exactly what exists and where it lives.

Add your insurance policies (life, disability, homeowners, auto) because your agent may need to pay premiums or file claims. This inventory takes a few hours now but saves your agent weeks of detective work later and prevents missed payments that damage your credit or allow policies to lapse. Pair this inventory with your healthcare situation by listing any chronic conditions, current medications, preferred doctors, and end-of-life preferences so your agent understands medical decisions that might affect your finances (long-term care costs, for example). Store this information in one place your agent can access quickly, whether that’s a shared digital folder, a binder at home, or with your attorney.

Define the Powers You Actually Grant

You must define the actual powers you grant because vague authority creates friction with banks and delays transactions when your agent needs to act fast. Florida law requires you to specify which powers you authorize rather than using blanket language, and financial institutions have four business days to accept or reject your POA if they question it. Do not grant powers you do not actually need because each additional authority increases your agent’s burden and potential liability.

If you only want someone to pay bills and manage bank accounts, state that explicitly rather than authorizing real estate sales, gifts, or trust creation that your agent will never use. However, if you own rental property or significant investments, grant specific authority over those assets so your agent can handle them without needing to petition a court for expanded powers later.

Understand Superpowers and Special Authorities

Certain superpowers in Florida require your initials next to each one: gifts to anyone (including the agent), creating or modifying trusts, changing beneficiary designations on insurance or retirement accounts, changing survivorship on bank accounts, and disclaiming property. These require deliberate action because they can redirect assets away from your intended heirs. If tax planning matters in your situation (business owners face this regularly), your agent needs explicit authority to file tax returns, work with your CPA, and make estimated payments so the IRS does not assess penalties against your estate.

Consider whether your agent should have investment authority because managing a diversified portfolio requires knowledge many family members lack. If your agent is not experienced with investments, limit that power or name a professional co-agent who handles only investments.

Align Your POA With Other Documents

Review any existing documents like wills, trusts, or beneficiary designations to ensure your POA does not contradict them because conflicting instructions between documents create expensive legal disputes your family will fight over after you are gone.

Final Thoughts on POA Planning

POA planning considerations require honest assessment of your financial situation, your agent’s capabilities, and how your documents work together. We at Family, Estate & Mediation Law have seen families avoid years of conflict and financial loss simply because someone took time upfront to think through these decisions carefully. The cost of proper planning now is minimal compared to the expense and heartache of fixing problems after a crisis hits.

Gather your financial inventory, identify the person you trust most to handle your affairs, and schedule a conversation with them about your expectations. Be specific about which powers you need, which ones you do not, and how you want your agent to manage your money. Review your will, trust, and beneficiary designations to confirm everything points in the same direction.

We at Family, Estate & Mediation Law work with individuals and families across Northeast Florida to build estate plans that actually work when you need them. Contact us to discuss your POA planning considerations and ensure your documents protect what matters most.