Most couples assume a single joint plan covers everything. That’s wrong, and it often leads to costly mistakes down the road.

Estate planning for couples requires separate strategies that protect each person’s individual wishes, assets, and legacy. At Family, Estate & Mediation Law, we’ve seen firsthand how poorly coordinated plans create conflict and tax problems that could have been prevented.

This guide walks you through what actually works.

Why Couples Need Separate Estate Plans

Most couples operate under a dangerous assumption: one joint will or trust protects both partners equally. Florida law doesn’t work that way, and this misconception costs families thousands in probate fees, taxes, and family conflict. Separate estate plans for each partner are non-negotiable because your assets, debts, and wishes are fundamentally different.

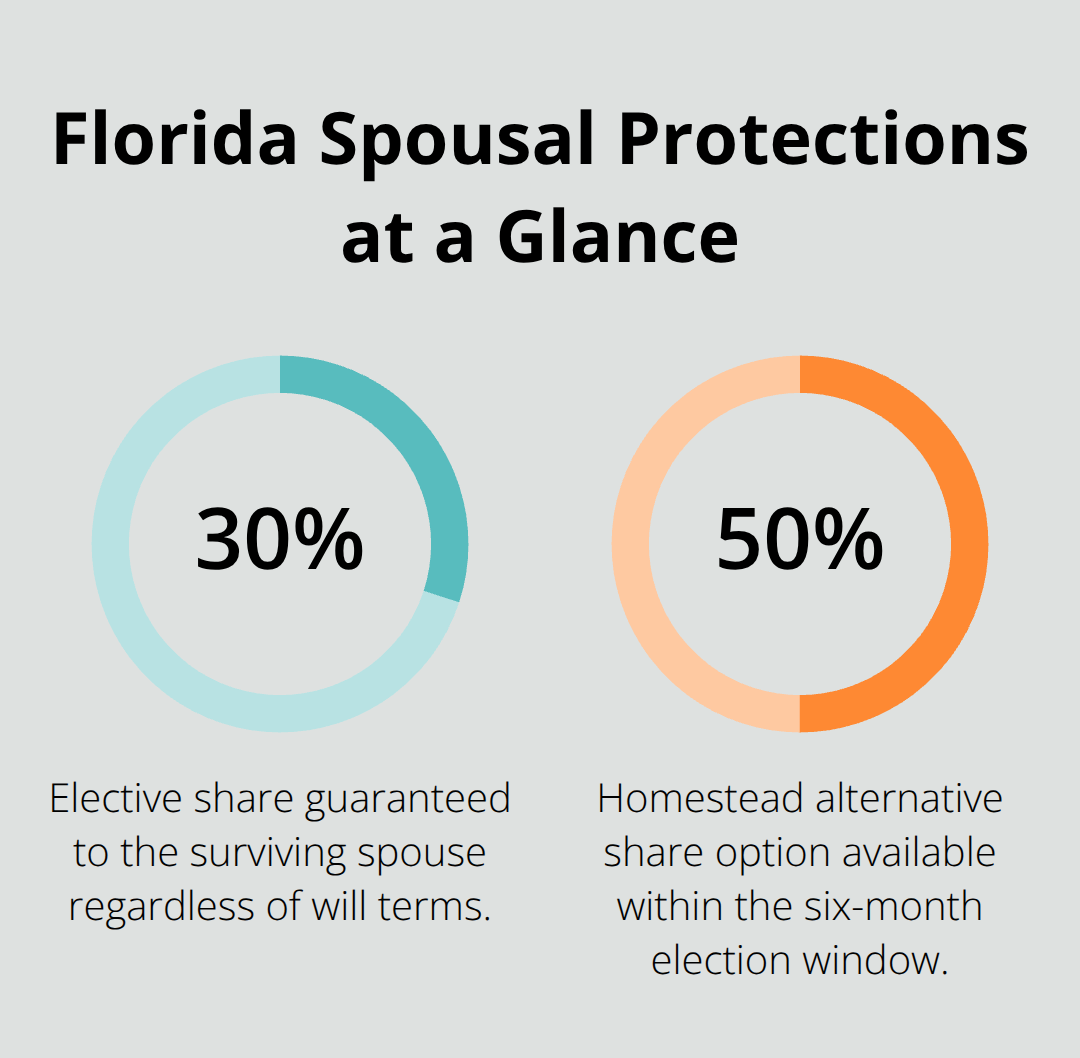

When one spouse dies, the surviving spouse’s legal rights are governed by Florida Statute 732.2075, which grants an elective share of 30 percent of the estate regardless of what a will says. If you leave less than 30 percent to your spouse through a joint plan, they can challenge it and claim that statutory share anyway. The result is a probate battle nobody wanted. Separate plans let each of you control your own legacy while accounting for Florida’s spousal protections.

Individual Assets Demand Individual Planning

A joint approach ignores the reality that you likely own property separately-a house from before the marriage, an inheritance, or a business one of you built. Commingling these assets in a single plan creates tax complications and muddies who actually owns what. Real property, retirement accounts, and life insurance all need separate beneficiary designations that align with each partner’s wishes.

If your 401(k) names your ex-spouse as beneficiary and you never updated it, that money bypasses your current spouse entirely. Your will cannot override a beneficiary designation. Audit all account titles and designations within the first 30 days of marriage or major asset changes to catch these problems early.

Florida homestead property adds another layer. If your home is titled as homestead and only one spouse is on the deed, the other spouse must sign to transfer it, even after death. A coordinated pair of separate plans addresses this upfront and prevents delays.

Blended Families Require Clear Separation

Blended families make individual planning even more critical. If you have children from a prior relationship and want to protect their inheritance while providing for a new spouse, a single joint plan guarantees conflict. Separate trusts for each partner, with clear instructions about which assets go to which children, prevent accidental disinheritance and reduce the likelihood of contested probate.

One partner’s separate property-say, inherited real estate-should transfer according to that partner’s wishes, not the other’s. Separate plans make this explicit and legally binding.

Each Partner’s Wishes Deserve Protection

Your spouse’s vision for your legacy is not your vision, and that’s okay. One of you may want to leave more to charity, while the other prioritizes grandchildren’s education funds. One may want assets in a trust for a surviving spouse’s lifetime, while the other prefers outright distribution. A joint plan forces compromise and often leaves both partners unsatisfied. Separate plans eliminate this tension.

Powers of Attorney and healthcare directives also demand individual attention. If you name the same agent for financial and medical decisions, and that person becomes incapacitated or unavailable, you have no backup. Each partner should name their own trusted agents for finances, healthcare, and end-of-life decisions. Florida no longer recognizes springing powers of attorney, meaning your document takes effect immediately upon signing-another reason to verify it reflects your current priorities.

Tax Planning Varies by Partner

Tax planning differs significantly by partner. If one spouse has substantially more income or assets, a coordinated strategy using trusts, lifetime gifts, and beneficiary designations can minimize federal estate taxes. With the current federal exemption at approximately $13 million per person, couples with combined estates above that threshold benefit enormously from separate, complementary plans. Without individual planning, you leave money on the table that could pass tax-free to your heirs.

The coordination of these separate plans-ensuring they work together rather than against each other-is where most couples stumble. This is where the real work of estate planning begins.

Key Components of Estate Plans for Couples

Revocable Living Trusts Form Your Foundation

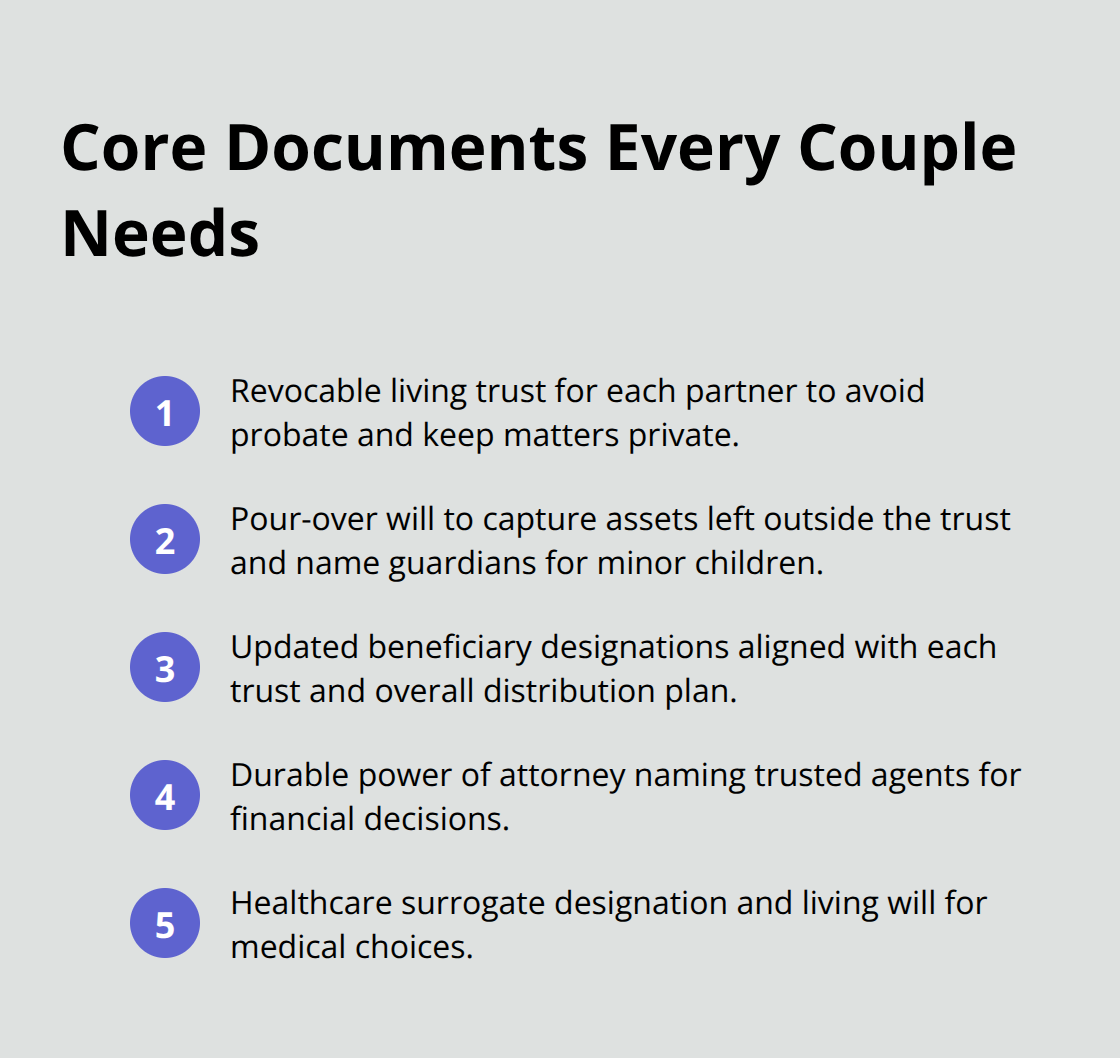

A solid estate plan for couples rests on four interlocking documents that work together to handle finances, healthcare, and asset transfer. Each partner needs a revocable living trust to avoid probate entirely for assets titled in its name. In Florida, probate moves slowly and exposes your family’s financial details to public record, so a trust-based approach keeps matters private and saves months of court delays plus thousands in fees. Each partner funds their own trust with separate property, retirement accounts, and beneficiary designations, then coordinates these documents so they complement rather than contradict each other.

A will serves as a safety net, directing any assets left outside the trust and naming guardians for minor children if both parents die simultaneously. Without a will, Florida’s intestacy laws decide who raises your kids-a decision you don’t want the state making.

Beneficiary Designations Demand Immediate Attention

Beneficiary designations on retirement accounts, life insurance, and bank accounts override what your will or trust says, so they require immediate attention. If you married or divorced within the last five years, audit every 401(k), IRA, and insurance policy to confirm the named beneficiary matches your current wishes. Many couples discover an ex-spouse still listed as beneficiary on a $500,000 life insurance policy, which means that money never reaches the surviving spouse or children. For couples, name each other as primary beneficiary on most accounts, then list your children or trust as contingent beneficiary in case you die simultaneously. Pay-on-death bank account designations transfer funds directly to named beneficiaries at death, bypassing probate entirely, though they offer less flexibility than a trust if circumstances change.

Powers of Attorney and Healthcare Directives Protect Your Autonomy

Each partner needs a durable power of attorney for financial decisions and a healthcare surrogate designation plus living will for medical choices. Florida no longer recognizes springing powers of attorney, meaning your financial power of attorney takes effect immediately upon signing, so only name someone you trust completely and review it annually to confirm they’re still the right choice. If you name the same agent for financial and medical decisions, and that person becomes incapacitated or unavailable, you have no backup. Each partner should name their own trusted agents for finances, healthcare, and end-of-life decisions to eliminate this vulnerability.

The coordination of these separate documents-ensuring they work together rather than against each other-determines whether your plan actually protects your shared future or creates conflict when you need it most.

Protecting Your Shared Future Without Conflict

Align Your Separate Plans to Eliminate Legal Conflicts

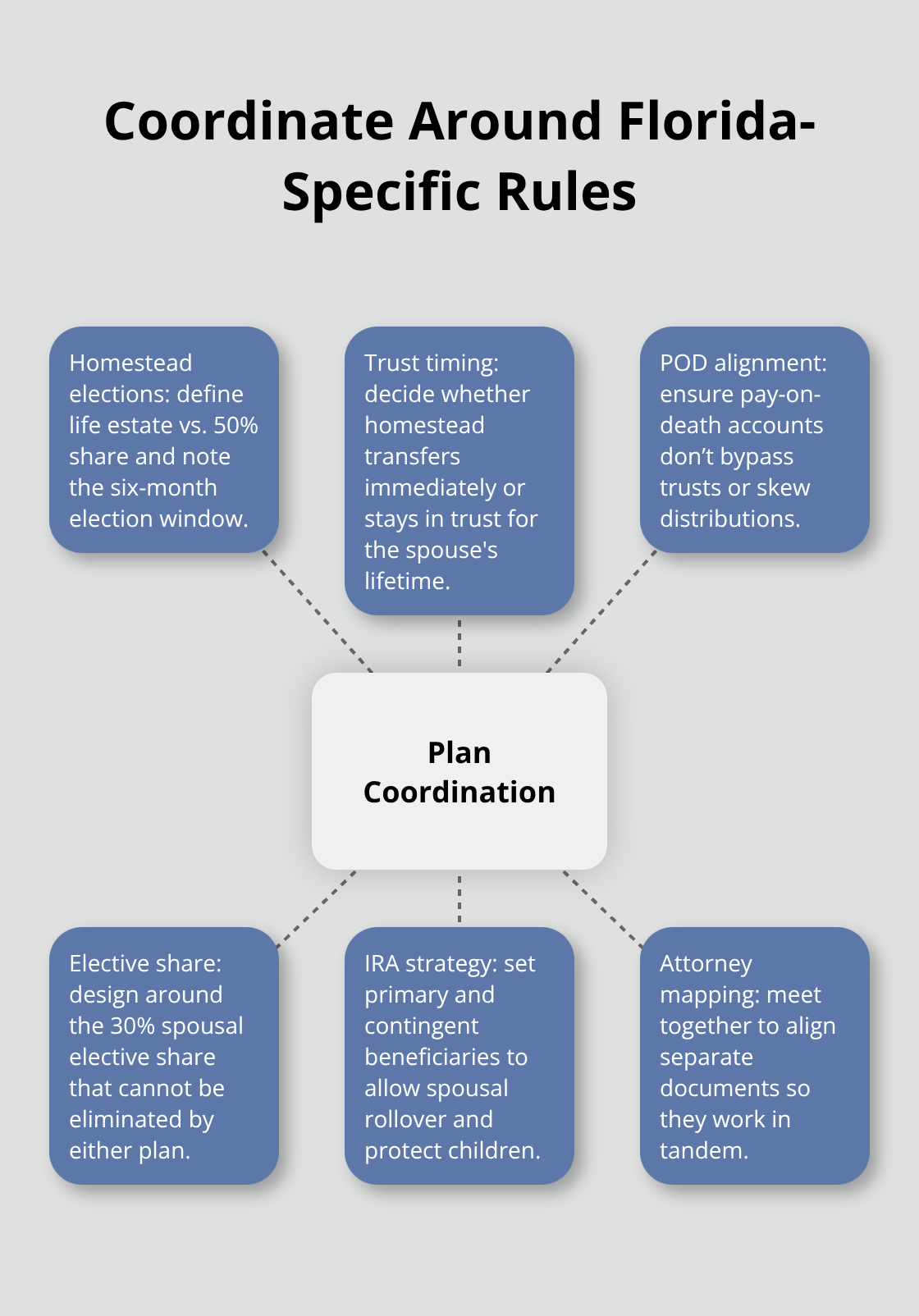

Coordination between separate plans determines whether your estate strategy protects your shared future or creates conflict when you need it most. Most couples fail at this step, and the consequences are expensive. When one spouse creates a will leaving everything outright to the surviving spouse while the other funds a trust that locks assets away for decades, conflicting documents emerge that probate judges will spend months untangling. The fix is straightforward but requires deliberate attention. Both partners must sit down together with an estate planning attorney to map out how your separate plans work in tandem.

If one spouse owns a home titled as homestead and the other owns investment property, your beneficiary designations and trust structures need to account for Florida’s homestead protections under Fla. Stat. 732.2075, which grants the surviving spouse a life estate or 50 percent share with a six-month election window. Your separate trusts should specify whether that homestead property transfers immediately or remains in trust for the surviving spouse’s lifetime. Pay-on-death designations on bank accounts should align with your overall distribution strategy so one account doesn’t bypass the trust entirely while another feeds into it.

The surviving spouse’s elective share of 30 percent cannot be eliminated by either plan, so coordinate around this reality rather than fighting it. Test your coordination by asking: if one partner dies tomorrow, does the surviving spouse receive what you both intend, or do conflicting documents create a probate mess? That question forces clarity.

Protect Children in Blended Family Situations

Blended families demand even tighter coordination because the stakes involve protecting children from prior relationships while providing for a new spouse. Separate trusts for each partner become non-negotiable here. One partner’s trust might direct that inherited real estate passes to adult children from a first marriage, while the other partner’s trust provides income to the surviving spouse but ensures the principal eventually reaches different beneficiaries. Without separate trusts with explicit instructions, a surviving spouse could claim the entire estate and disinherit your children entirely.

Life insurance proceeds require careful planning in blended situations. If you carry a $750,000 policy and name your current spouse as beneficiary, your adult children receive nothing unless you’ve structured a trust that captures those proceeds and distributes them according to your wishes after your spouse’s death. Name the trust as beneficiary, not the spouse directly, and your plan survives remarriage or relationship changes.

Structure Tax-Efficient Coordination for Your Combined Estate

Tax planning in couples’ situations varies dramatically based on combined assets and income. With the federal estate tax exemption currently at approximately $13 million per person, couples with combined estates above $26 million benefit enormously from coordinated lifetime gifting strategies and trust structures that split assets between separate trusts. If your estate falls below that threshold, the priority shifts to probate avoidance and privacy rather than federal tax reduction.

Coordinate your beneficiary designations on retirement accounts so that if one spouse dies with a large IRA, the surviving spouse can roll it into their own account and continue tax-deferred growth. A contingent beneficiary designation protects your children if both spouses die simultaneously. These coordination points separate a functional plan from an expensive disaster.

Final Thoughts

Estate planning for couples succeeds when both partners commit to separate, coordinated strategies that reflect individual wishes while protecting shared assets. The foundation rests on four documents working in tandem: revocable living trusts for each partner, beneficiary designations aligned with your overall plan, powers of attorney naming trusted agents, and healthcare directives that specify end-of-life preferences. Without this coordination, conflicting documents create probate delays, tax complications, and family conflict that could have been prevented.

Start by auditing every account title, beneficiary designation, and property deed to identify gaps between your current wishes and what’s actually documented. If you own homestead property, confirm both spouses understand Florida’s statutory protections and how they affect your plan. If you have children from prior relationships, separate trusts become non-negotiable to protect their inheritance while providing for a surviving spouse (and if your combined estate exceeds $26 million, coordinate lifetime gifting strategies and trust structures to minimize federal taxes).

We at Family, Estate & Mediation Law help couples across Northeast Florida build estate plans that actually work. Contact us today at our offices in St. Augustine and Palatka to start your estate planning for couples.