Remarriage brings joy, but it also creates legal complications your old will likely doesn’t address. When you marry again, your estate plan becomes outdated almost immediately, leaving your blended family vulnerable to disputes and unintended consequences.

At Family, Estate & Mediation Law, we see this problem constantly. Wills updated for remarriage aren’t optional-they’re essential protection for everyone in your household.

Your Old Will Probably Doesn’t Include Your New Family

A will you signed before remarriage treats your new spouse and stepchildren as strangers, regardless of how central they’ve become to your life. Florida law doesn’t automatically update your intentions when you marry again-your documents remain frozen in time, creating a dangerous mismatch between your actual family and what your estate plan recognizes. If your previous will named only your biological children as beneficiaries or left everything to your first spouse, that language stays in effect unless you actively change it. Stepchildren have zero automatic inheritance rights under Florida Statute 732.103, even if you’ve raised them since they were infants.

How State Law Can Undermine Your Intentions

Your current spouse faces similar problems if your will predates the marriage. Florida courts won’t guess what you would have wanted, and they won’t rewrite your documents to reflect your new circumstances. This isn’t theoretical-families split apart annually because a parent remarried but never updated their will, leaving a surviving spouse with inadequate support and prior children feeling betrayed by unexpected distributions.

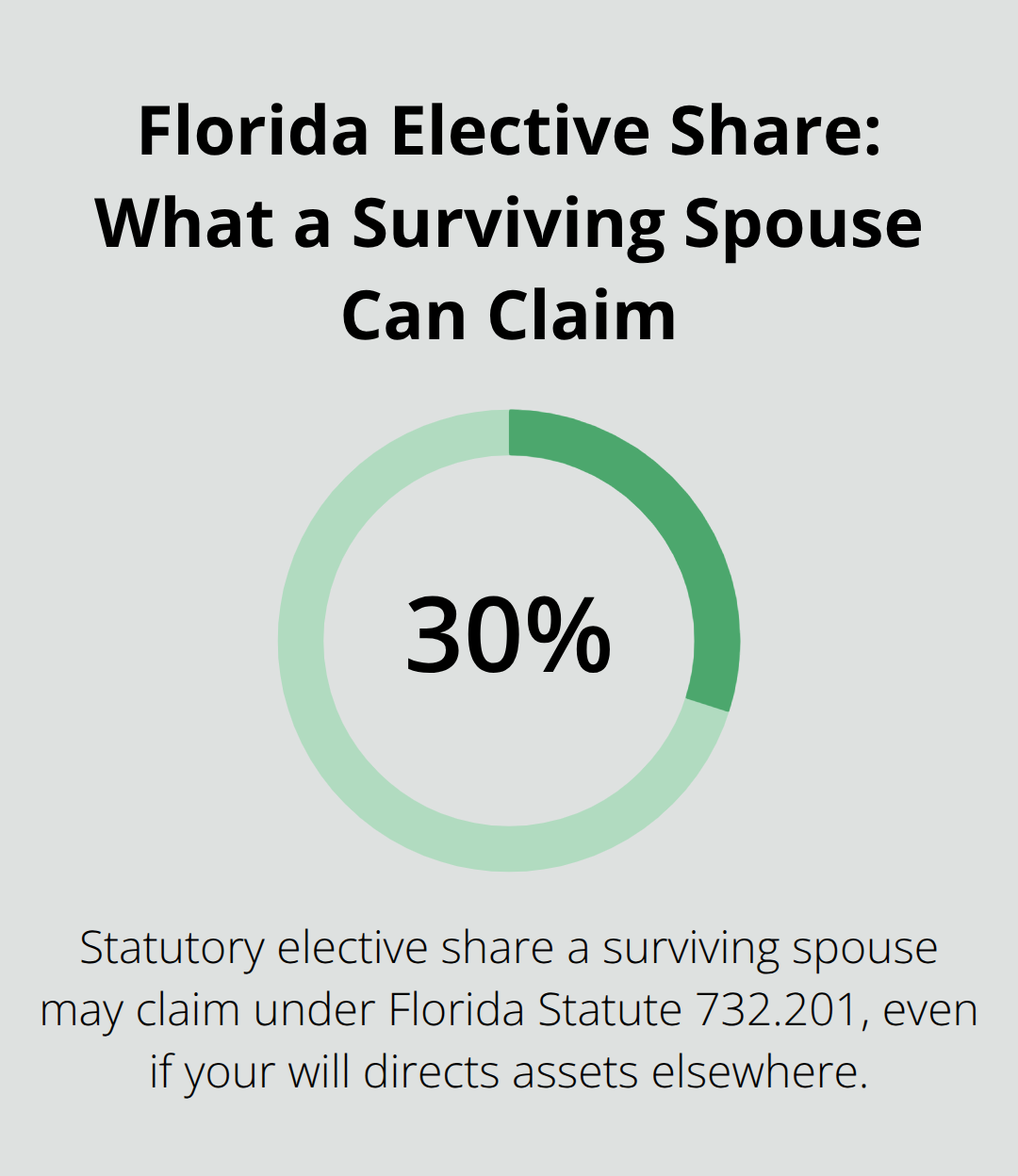

Florida’s elective share law complicates blended-family planning further. A surviving spouse can claim 30% of your estate under Florida Statute 732.201, even if your will directs assets elsewhere. This means your carefully planned bequests to biological children from a prior marriage can be overridden by a spouse’s legal claim, creating exactly the conflict you wanted to prevent.

If you die intestate (without a valid will), Florida intestacy rules prioritize your surviving spouse and biological or adopted children-stepchildren receive nothing. In scenarios where all your children are also your current spouse’s children, the spouse could inherit your entire estate, leaving no protection for adult stepchildren or grandchildren from prior relationships. Your remarriage also potentially invalidates assumptions in your old will; if that document assumed your first spouse would raise the children or manage assets, those provisions now make no sense. Florida courts apply outdated language literally, which frequently produces results you never intended.

Beneficiary Designations Override Your Will Entirely

Life insurance policies, retirement accounts, and payable-on-death bank accounts pass directly to named beneficiaries and completely bypass your will. If your policy still names an ex-spouse or a deceased beneficiary, that designation controls the payout, not your updated will. Retirement accounts like IRAs and 401(k)s represent a significant portion of most people’s wealth, yet many fail to update beneficiary forms after remarriage.

This means your new spouse might inherit nothing from your largest assets while stepchildren you intended to support receive nothing either. Conduct a complete audit of every account that has a beneficiary designation-bank accounts, brokerage accounts, life insurance, retirement plans, and even some annuities. List the current beneficiary on each one and compare it to your actual intentions.

If you’ve remarried and haven’t touched these designations in years, they almost certainly don’t reflect your blended family’s needs. Updating beneficiary forms takes minutes and costs nothing, yet this single step prevents more estate disputes than almost any other action. Once you’ve identified which documents need changes, you’ll need to address the larger question of how to structure distributions that protect both your current spouse and your children from prior relationships.

How to Structure Asset Distribution in Your Updated Will

Deciding who receives what after you pass away becomes infinitely more complex when your family includes both biological children and stepchildren. Start with a complete asset inventory that lists every account, property, investment, and piece of personal property you own, then assign each item a specific destination. This isn’t about treating everyone equally-it’s about treating everyone fairly according to your actual values.

Many remarried parents mistakenly assume their will automatically protects both groups, but Florida law gives stepchildren zero inheritance rights unless you explicitly name them. If you want a stepchild to receive your home, retirement account, or a specific heirloom, write it down with their full legal name and exact relationship to you. Vague language like “my children” creates ambiguity that probate courts resolve by excluding stepchildren entirely.

Structuring Distributions Between Spouse and Children

Your will should specify whether your surviving spouse receives assets outright or holds them in trust for your children’s benefit after their death. This distinction matters enormously. If your spouse inherits your entire estate outright, they can legally redirect it to their own biological children or a new partner, completely bypassing your children from a prior marriage.

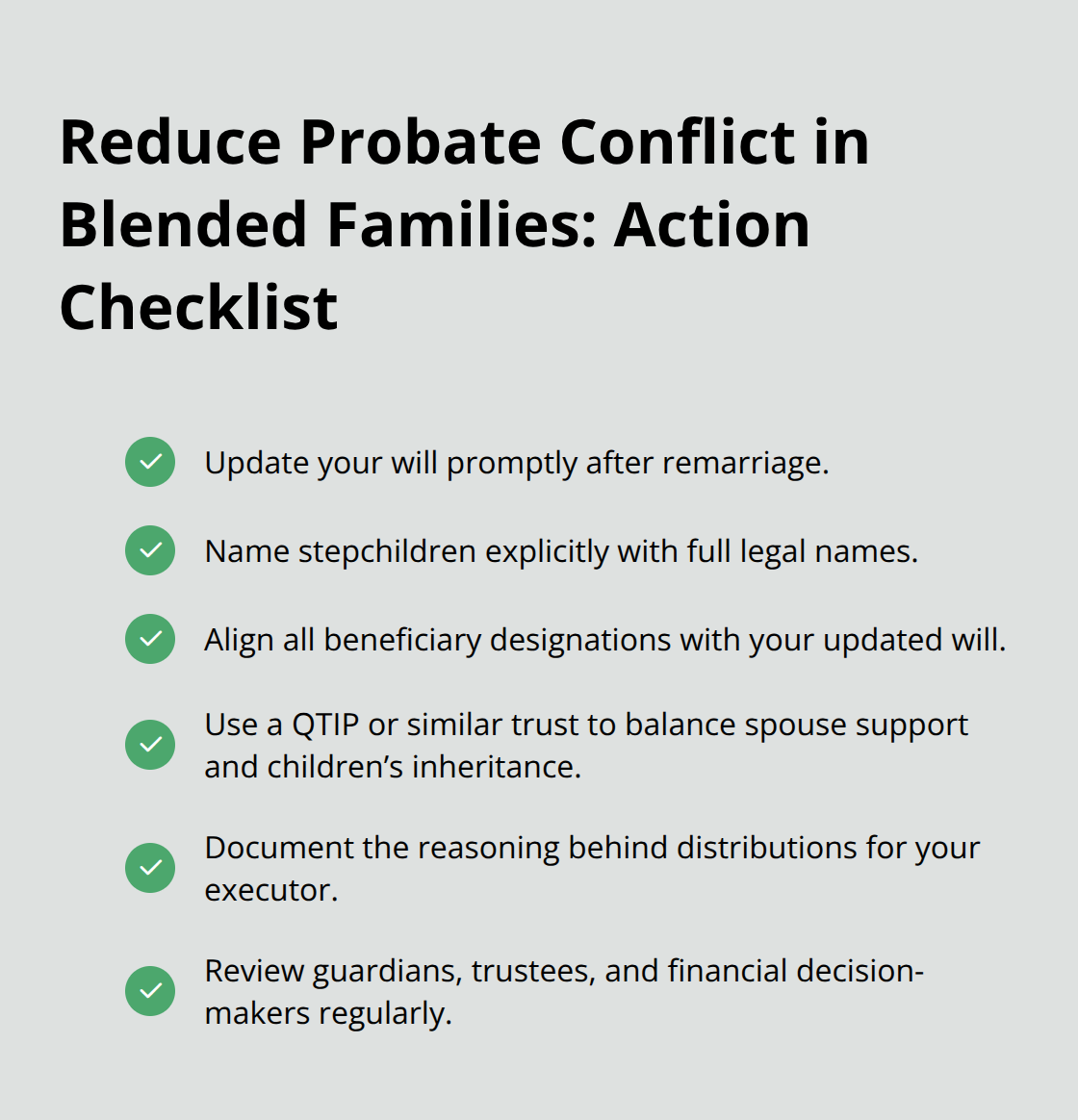

A more protective structure uses a QTIP trust, which provides income to your spouse during their lifetime while preserving the principal for your designated heirs. This approach balances your spouse’s financial security with your children’s inheritance rights. For blended families with unequal asset distribution between spouses, consider whether each partner should leave assets to their own biological children or whether combined assets should be divided by family line. Document your reasoning so your executor understands your intentions if disputes arise.

Naming Guardians and Decision-Makers for Minor Children

If you have minor children from a previous relationship, your will must explicitly name a guardian who will raise them if both you and your current spouse die simultaneously or in quick succession. This decision cannot be left to chance or assumed. Florida courts will appoint a guardian based on the child’s best interests, which may not align with your wishes if you haven’t documented them.

Your will should name a primary guardian and at least one alternate in case your first choice is unable or unwilling to serve. Many remarried parents fail to update guardian nominations from their first marriage, leaving outdated choices in effect. If your previous will named your ex-spouse as guardian, that designation likely remains valid unless you explicitly revoke it and name someone else. You also need to designate who manages finances for your minor children-this person might differ from the guardian who raises them. A financial guardian or trustee handles money and property until the child reaches adulthood, making this role equally critical. Your will should specify how much discretion the guardian has regarding education, healthcare, extracurricular activities, and spending decisions. These provisions prevent conflicts between your guardian and your current spouse, who may have different parenting philosophies or financial priorities.

Updating Every Beneficiary Form Outside Your Will

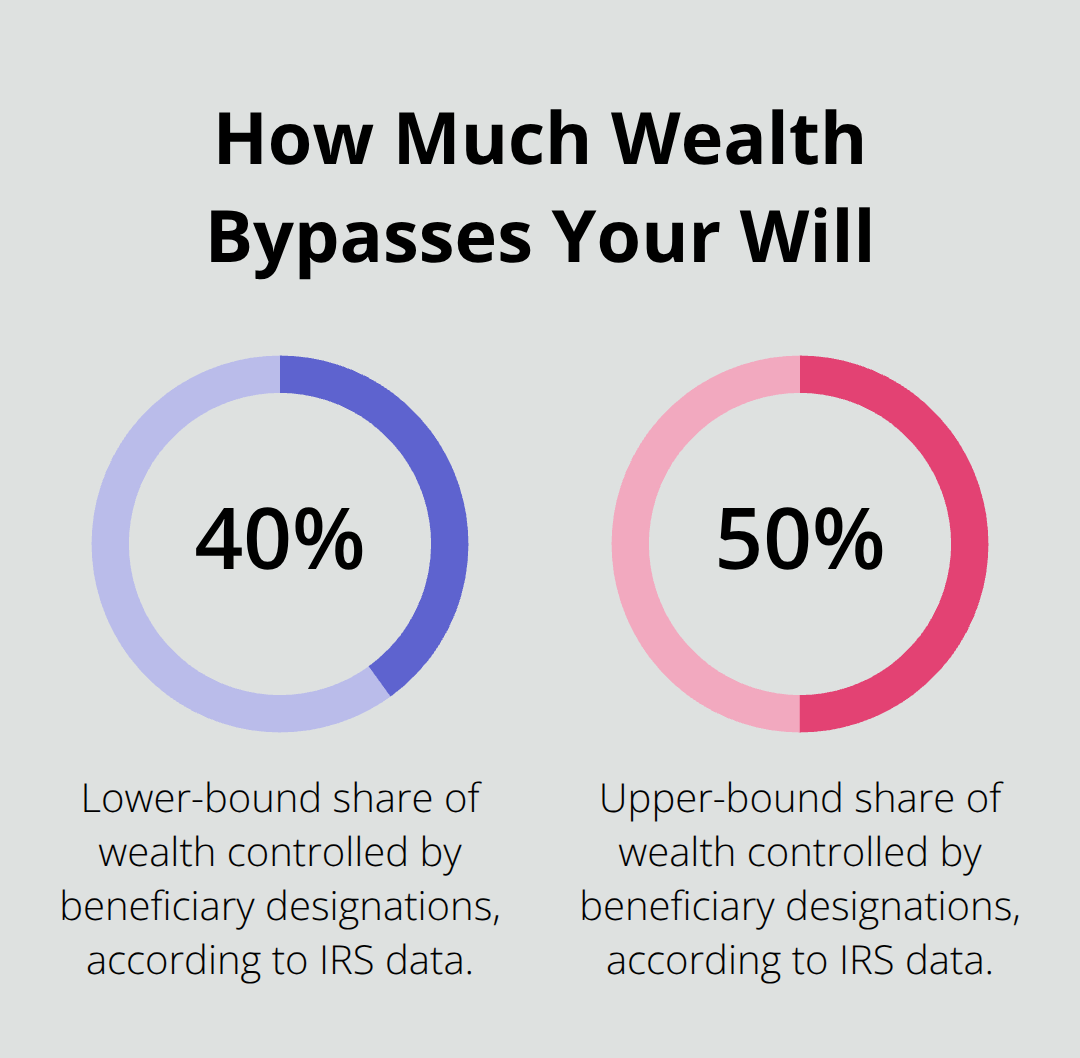

Retirement accounts, life insurance policies, and payable-on-death designations control approximately 40 to 50 percent of most Americans’ wealth according to IRS data, yet these assets bypass your will entirely and pass directly to whoever you named as beneficiary. If you’ve remarried since opening these accounts, the beneficiary forms almost certainly need updating.

Contact your employer’s HR department, your financial institutions, and your insurance providers to request current beneficiary information for every account you own. Create a spreadsheet listing the account type, current beneficiary, and your intended beneficiary for each one. Many people discover that outdated designations still name an ex-spouse, a deceased parent, or a former employer’s plan administrator. Updating beneficiary forms takes minutes and costs nothing, yet this single action prevents more estate disputes than nearly any other step.

If you want your current spouse to receive life insurance proceeds but your biological children to eventually inherit retirement accounts, document this in writing and ensure the beneficiary forms reflect it exactly. Some people use beneficiary designations strategically by naming different heirs for different assets-for example, naming your spouse as beneficiary of liquid accounts but your children as beneficiaries of retirement plans. This approach requires careful coordination with your overall estate plan to avoid accidentally disinheriting someone or creating unequal distributions you didn’t intend. Once you’ve updated your will and beneficiary designations, you’ll want to address whether additional legal protections-such as prenuptial or postnuptial agreements-make sense for your specific situation.

What Happens When Your Will Ignores Your Blended Family

Stepchildren and biological children face dramatically different legal outcomes when your will fails to address your blended family-and most remarried parents have no idea how exposed their families actually are. Stepchildren inherit absolutely nothing under Florida law unless you explicitly name them in your will or trust, regardless of how long you’ve raised them or how central they’ve become to your life. Florida Statute 732.103 is unambiguous: stepchildren don’t qualify as heirs during intestate succession, meaning if your will contains gaps or ambiguities, courts resolve them by excluding stepchildren entirely. This isn’t a technicality-it’s the default outcome when documentation fails to address blended-family realities.

How Your Surviving Spouse Can Redirect Your Children’s Inheritance

Your biological children face the opposite problem: a surviving spouse who inherits assets outright can legally redirect everything to their own children or a new partner, leaving your prior children with nothing despite your intentions to provide for them. One scenario we see repeatedly involves a parent who updated their will to include their new spouse but failed to address how assets pass after that spouse dies. This mistake accidentally creates a structure where the surviving spouse controls the entire inheritance rather than your children receiving their share.

The financial impact is substantial. According to data from the American Academy of Matrimonial Lawyers, over 40 percent of blended families report significant conflict over inheritance when the deceased parent failed to update their estate documents after remarriage. Your current spouse also faces inadequate financial protection if your will was drafted before the remarriage, since provisions written for a first spouse don’t account for your new partner’s actual needs or lifestyle.

The True Cost of Probate Disputes in Blended Families

Probate disputes in blended families consume enormous time and money precisely because outdated wills create legal ambiguity that courts must resolve through expensive litigation. When a will names only biological children but the deceased had been married for fifteen years to someone raising stepchildren, the surviving spouse often challenges the will, arguing they deserve more than the document provides or that the deceased’s intentions changed. These disputes routinely cost $50,000 to $150,000 in attorney fees before resolution, draining assets that should have passed to heirs and creating permanent rifts between family members.

A widowed spouse who receives insufficient income from inherited assets may need to sell property to cover living expenses, forcing the sale of homes or businesses that your biological children expected to inherit intact. This scenario plays out repeatedly: a surviving spouse struggles financially while adult children from prior relationships watch family assets liquidate to cover their stepparent’s costs.

Fixing the Problem With Specific Language

The solution requires deliberate, specific language in your will that addresses how much each spouse receives, whether stepchildren benefit during the surviving spouse’s lifetime or only afterward, and whether certain assets remain protected for your biological children’s inheritance. Without this specificity, Florida probate courts apply intestacy principles to fill gaps, which systematically favors the surviving spouse over stepchildren and often produces distributions that contradict your actual wishes. Your will should name stepchildren explicitly with their full legal names and specify exactly what they receive. Beneficiary designations on retirement accounts, life insurance, and bank accounts override what your will says, so they require immediate attention. Vague language like “my children” creates ambiguity that probate courts resolve by excluding stepchildren entirely, so precision matters more in blended families than in any other estate planning scenario.

Final Thoughts

Remarriage transforms your family structure, and your estate plan must reflect that reality. Wills updated for remarriage protect everyone you care about by eliminating the legal ambiguity that creates disputes, disinheritance, and financial hardship. Without deliberate updates, your surviving spouse may struggle financially while stepchildren receive nothing, or your biological children’s inheritance could shift to a surviving spouse’s own family line.

Probate disputes in blended families destroy relationships between stepparents and stepchildren and consume resources that should pass to heirs. Your current spouse deserves financial security, your biological children deserve clarity about their inheritance, and your stepchildren deserve to know whether you intended to provide for them. State law does not automatically address these outcomes through outdated documents.

Schedule a consultation with Family, Estate & Mediation Law to review your current documents and identify what needs updating. Bring your asset inventory and beneficiary forms, and be honest about your intentions for each family member. This conversation takes a few hours now and prevents decades of conflict later.