Most Florida residents put off estate planning because they think it’s only for the wealthy or elderly. The truth is far different-without a solid plan, your family faces probate delays, unnecessary costs, and uncertainty about your wishes.

At Family, Estate & Mediation Law, we help people in St. Augustine and Palatka understand the basics of estate planning and build protection that actually works. This guide walks you through the essential documents, common mistakes, and practical steps to get started today.

Why Estate Planning Matters in Florida

Probate Costs and Delays Hit Your Family Hard

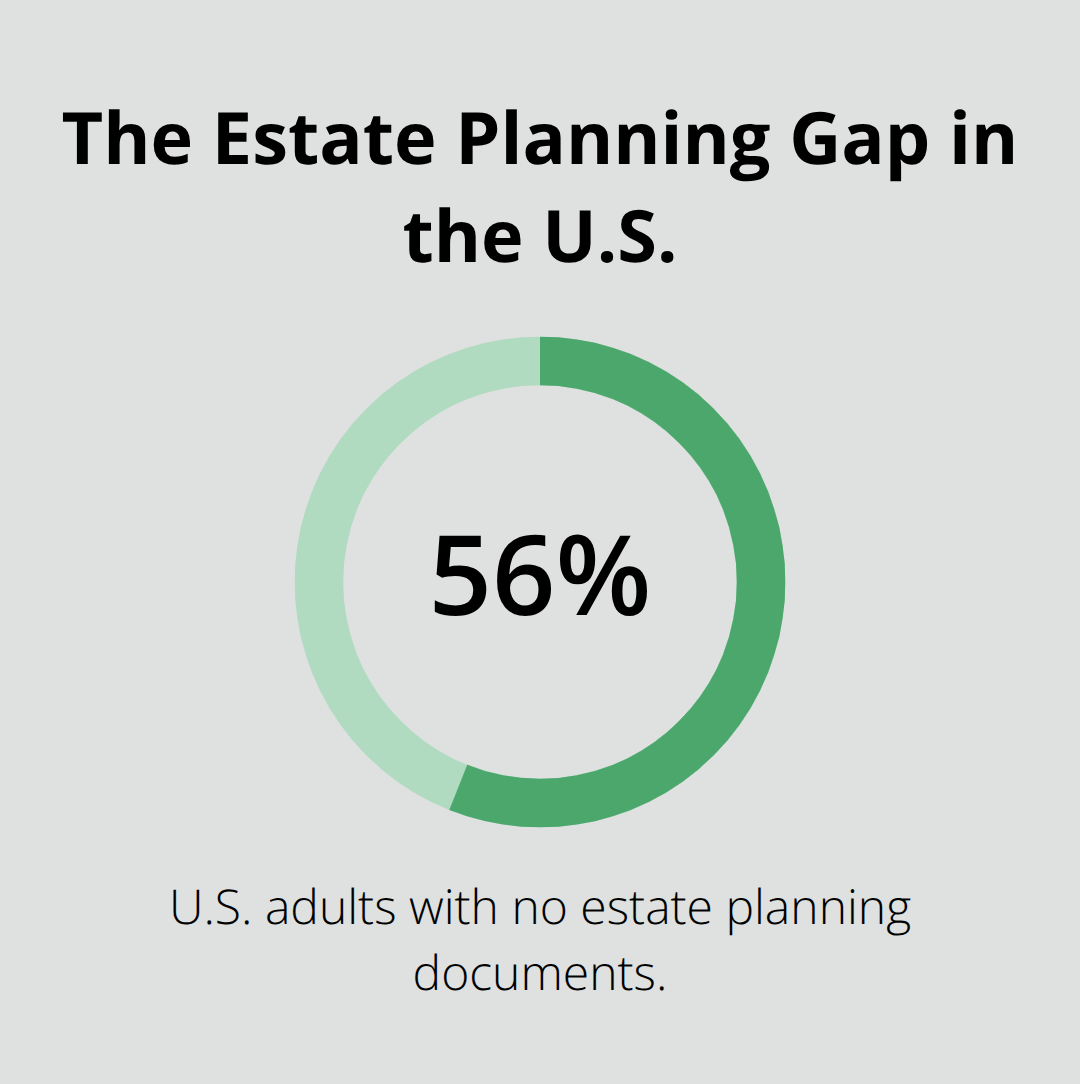

Probate in Florida costs money and time that your family simply doesn’t need to waste. According to Trust and Will’s 2026 Estate Planning Report, 56% of U.S. adults have no estate planning documents at all, which means their families face court proceedings that can take months or even years. During probate, your estate pays court fees, attorney fees, and executor fees-costs that easily reach thousands of dollars depending on your asset size.

Without a plan, your family also loses privacy since probate records become public. Probate delays create stress when families need liquidity most, such as paying outstanding debts or covering living expenses while waiting for asset distribution.

Your Wishes Control the Outcome, Not Florida Law

Without a clear estate plan, Florida law decides how your assets get distributed, and that outcome might not match your actual wishes. A revocable living trust keeps your assets outside probate entirely, but only if you properly fund it with your property titles and accounts. The difference matters: assets in a trust pass directly to your beneficiaries within weeks, while probate assets sit frozen for months.

Beneficiary Designations Override Everything Else

Beneficiary designations on retirement accounts and life insurance policies override what your will says, so outdated designations cause real problems. A 2013 Supreme Court decision in Hillman v. Hillman showed that failing to update beneficiary designations after divorce can award your retirement savings to an ex-spouse, not your current family. Transfer-on-death accounts and payable-on-death designations let you name beneficiaries for bank accounts and brokerage accounts without trusts, giving you flexibility while maintaining full control during your lifetime.

Tax Planning Protects Your Wealth

The 2026 federal estate tax exemption rises to $15 million per individual, which means fewer Florida residents face federal taxes, but state-specific planning still protects your wealth from unnecessary erosion through probate costs and delays. With proper planning in place, you move forward to selecting the specific documents that form the backbone of any solid estate plan.

Essential Documents That Protect Your Florida Estate

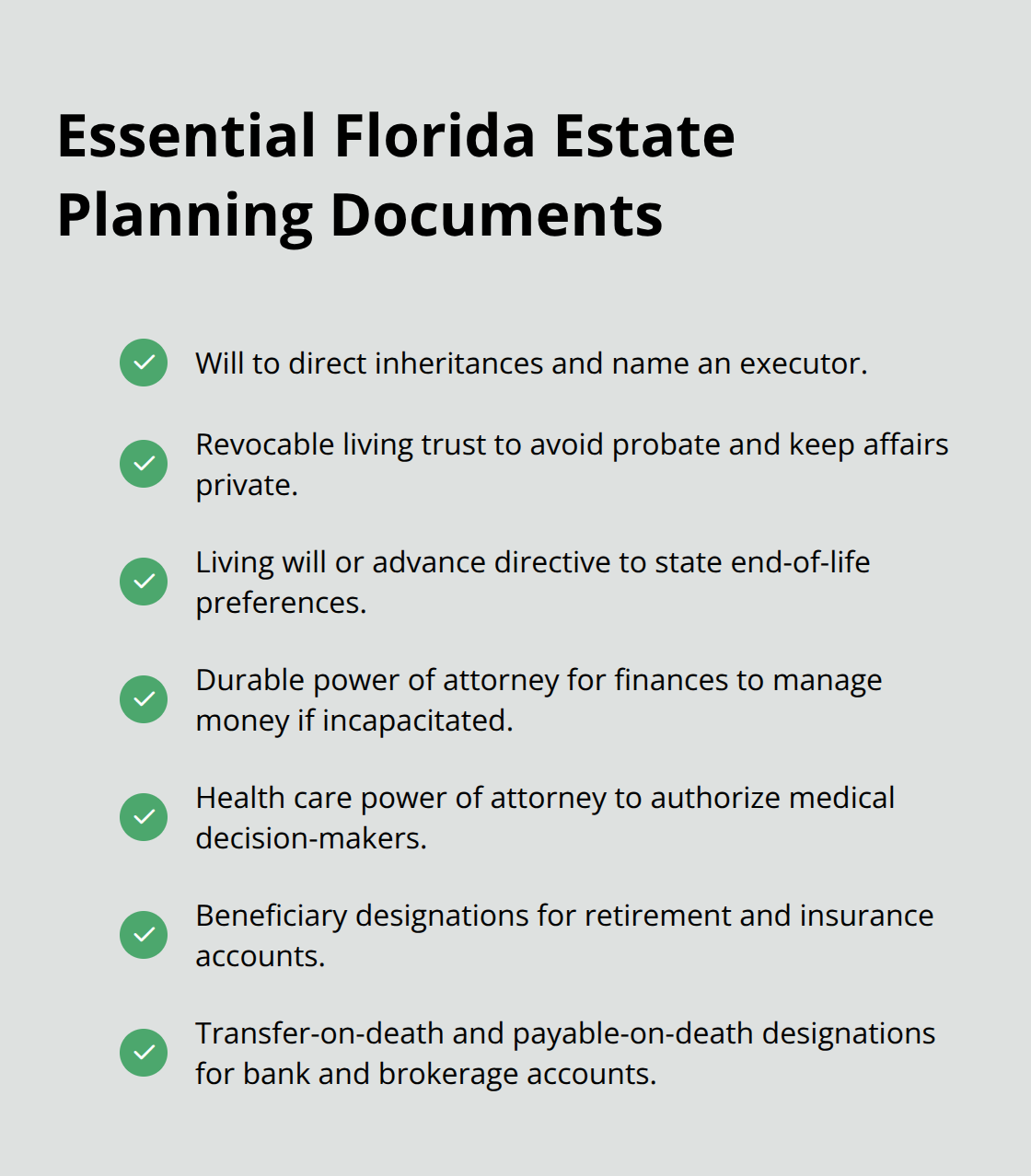

A will alone leaves your family vulnerable to probate court delays and public disclosure, which is why multiple documents working together form the backbone of any solid estate plan. Your will names who inherits what and appoints an executor to carry out your wishes, but it only controls assets titled in your individual name-everything else passes outside your will through beneficiary designations, joint ownership, or trust provisions. A revocable living trust holds title to your property during your lifetime and transfers assets directly to beneficiaries after your death without probate, avoiding months of court proceedings and keeping your affairs private. The National Council on Aging’s Estate Planning Guide emphasizes that a solid plan typically includes a will, a revocable living trust, a living will or advance directive, a durable power of attorney for finances, and a health care power of attorney. For retirement accounts like 401(k)s and IRAs, beneficiary designations override your will entirely-a 401(k) passes to your surviving spouse by default unless your spouse signs a waiver, while IRAs let you name non-spouse beneficiaries depending on state rules.

Transfer-on-death accounts and payable-on-death designations on bank and brokerage accounts bypass probate for those specific assets while keeping them under your control until death.

Powers of Attorney Handle Finances When You Cannot

A durable power of attorney for finances names someone to manage your bank accounts, investments, and property if you become incapacitated or unable to handle decisions yourself. This document takes effect immediately or upon incapacity depending on how you structure it, and it remains valid even if you become mentally incompetent-unlike a regular power of attorney that terminates if you lose capacity. Without one, your family must petition the probate court for guardianship, a costly and public process that takes weeks or months while your bills go unpaid and your accounts sit frozen. You should name both a primary agent and successor agents in case your first choice becomes unavailable or unwilling to serve.

Healthcare Directives and Living Wills Guide Medical Decisions

A healthcare power of attorney names someone to make medical decisions if you cannot communicate your wishes, while a living will documents your specific preferences about life support and end-of-life care. These documents prevent family disputes over treatment and spare your loved ones from guessing what you would have wanted during a medical crisis. Florida law recognizes both documents as legally binding, and many hospitals require them before admission. You should review these documents every three to five years or after major health changes, since medical technology and your own wishes may shift over time.

Beneficiary Designations Demand Constant Attention

Beneficiary designations on retirement accounts, life insurance policies, and transfer-on-death accounts override what your will says, so outdated designations cause real problems. A 2013 Supreme Court decision in Hillman v. Hillman showed that failing to update beneficiary designations after divorce can award your retirement savings to an ex-spouse, not your current family. You must add contingent beneficiaries to avoid unintended transfers if your primary beneficiary dies before you do. Life changes like marriage, divorce, or the birth of children require you to review and update these designations immediately-waiting creates unnecessary risk for your family.

What Happens When You Don’t Update Your Estate Plan

Life Changes Demand Immediate Action

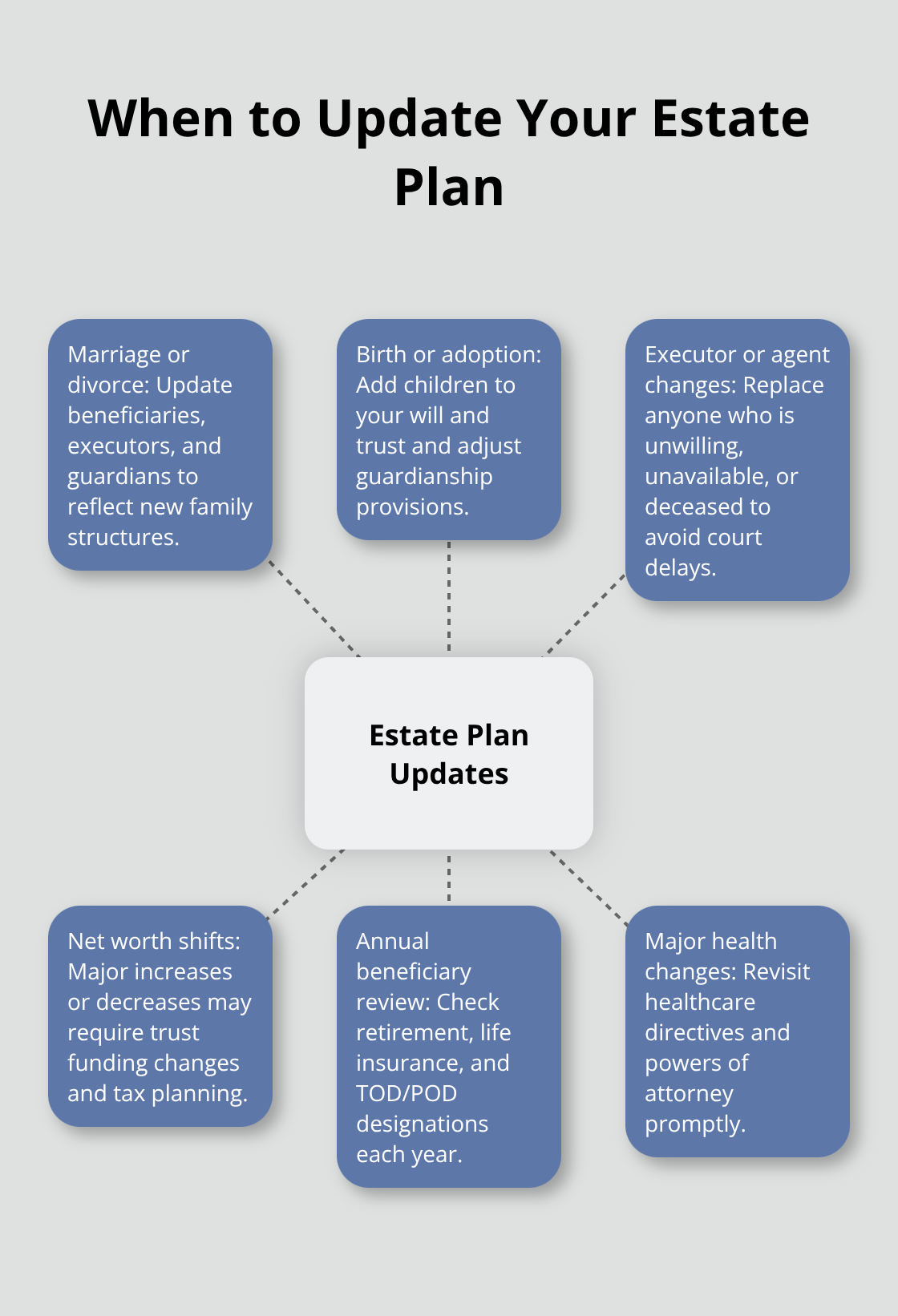

Life shifts faster than most people realize, and your estate plan needs to move with it. Divorce, remarriage, the birth of children or grandchildren, significant changes in your asset value, and the death of named beneficiaries or executors all require immediate updates to your documents. The Hillman v. Hillman Supreme Court decision remains a stark reminder of what happens when you ignore this rule: a man died with his ex-wife still named as beneficiary on his retirement account, and she received hundreds of thousands of dollars that he intended for his current family.

Florida residents commonly assume their will automatically updates after major life events, but it does not. Your beneficiary designations on 401(k)s, IRAs, life insurance policies, and transfer-on-death accounts operate independently from your will and trust, which means an outdated designation can override everything else you intended. A spouse who remarries without updating beneficiaries may accidentally leave assets to an ex instead of protecting the new family. Parents who fail to add newborn children to their wills create situations where those children inherit nothing unless the will explicitly names them or uses language like “all my children, whether born before or after this will.”

Executor Changes Create Court Complications

If you name your brother as executor and he dies before you do, your will still names him, which forces your family into probate court to have a judge appoint a replacement. This delay costs money and time that your family cannot afford to waste during an already stressful period. You should schedule a document review every three to five years at minimum, and update immediately after marriage, divorce, the birth or adoption of children, significant increases or decreases in your net worth, or the death of anyone named in your plan.

Keep a simple log of major life events and set calendar reminders to review your beneficiary designations annually, particularly on retirement accounts where errors prove most costly.

Underestimating Your Estate Value Leaves Families Unprotected

Many Florida residents believe estate planning only matters if they own a home, substantial investments, or a business, but the value of your assets adds up faster than you think. Your home in St. Augustine or Palatka likely represents significant equity, and when combined with retirement accounts, life insurance death benefits, vehicles, and personal property, the total often exceeds what people initially estimate. A $500,000 life insurance policy alone pushes your taxable estate into ranges where proper planning prevents unnecessary costs and delays.

Florida law allows a surviving spouse to claim an elective share of your estate, which means even with a will in place, your spouse may have independent legal rights that override your wishes unless you structure your plan specifically to address these provisions. The 2026 federal estate tax exemption of $15 million per individual currently protects most Florida families from federal taxes, but state-level probate costs and delays apply regardless of exemption thresholds. Someone with a $300,000 estate still faces thousands in probate fees, court costs, and months of delay if they lack a revocable living trust or other probate-avoidance strategies.

Digital Assets Compound the Problem

Digital assets compound this problem: cryptocurrency holdings, online business accounts, valuable social media profiles, and digital files hold real monetary or sentimental value that most people never list in their asset inventory. A comprehensive estate plan requires you to document everything you own, including partial interests in partnerships or family businesses, investment accounts, precious metals, and retirement benefits. This inventory becomes the foundation for deciding which assets go into a trust, which ones use transfer-on-death designations, and which ones require special tax planning to protect your family’s inheritance.

Getting Started Today

The basics of estate planning require you to take action, not wealth or age. Start by listing what you own: your home, vehicles, bank accounts, retirement accounts, investment accounts, life insurance policies, and any business interests, along with account numbers, current values, and current beneficiary designations. This inventory reveals gaps in your planning and shows exactly what needs protection.

Next, identify the people you trust most to manage your finances if you become incapacitated, make medical decisions for you, inherit your assets, and serve as executor. These decisions form the backbone of every estate plan and prevent family conflict and court intervention. Most people benefit from starting with a will, a revocable living trust, a durable power of attorney for finances, and healthcare directives (with beneficiary designations and transfer-on-death accounts following afterward).

We at Family, Estate & Mediation Law help Northeast Florida residents turn these decisions into legally binding documents that work. Contact us to review your current situation and identify which documents you need first, then set a calendar reminder to review your plan every three to five years and immediately after major life changes. Visit Family, Estate & Mediation Law to learn more about protecting your family’s future.