An irrevocable trust in Florida is one of the most powerful tools for protecting your assets and controlling your family’s financial future. Once you sign the documents, you cannot change your mind-which is exactly why these trusts work so effectively.

At Family, Estate & Mediation Law, we help clients in St. Augustine and Palatka understand when locking in your legacy through an irrevocable trust makes sense for your situation.

What an Irrevocable Trust Actually Is and How It Functions

An irrevocable trust in Florida is a legal arrangement where you transfer ownership of your assets to a trustee who then manages them for your beneficiaries. The defining feature is permanent: once created, you cannot revoke, amend, or take back what you’ve placed inside. Under Florida law, any trust is assumed revocable unless the document explicitly states otherwise. This means you must be intentional about creating an irrevocable structure from the start. The trustee holds legal title to the assets and has a fiduciary duty to follow the trust terms exactly as written, without deviation based on your changing preferences. Three ways to create an irrevocable trust in Florida are designating it as irrevocable at creation, allowing a revocable trust to become irrevocable upon your death, or establishing one through your will as a testamentary trust.

The Core Difference from Revocable Trusts

A revocable trust lets you maintain control during your lifetime. You can amend it, withdraw assets, or revoke it entirely if circumstances change. You typically serve as your own trustee, managing the assets yourself. An irrevocable trust strips away that control permanently. Once assets move into an irrevocable structure, they belong to the trust, not to you. This loss of control is actually the source of the protection. Because you no longer own the assets, they are shielded from your future creditors and lawsuits. Revocable trusts provide no such creditor protection during your lifetime since the law treats them as your personal property. The trade-off is clear: surrender control now to gain protection later. For Medicaid planning specifically, Florida’s five-year look-back period means assets transferred to an irrevocable trust must remain there untouched for sixty months before you qualify for benefits. If you transfer assets sooner, Medicaid penalizes you. This is why timing matters enormously in irrevocable planning.

How Florida Law Structures These Trusts

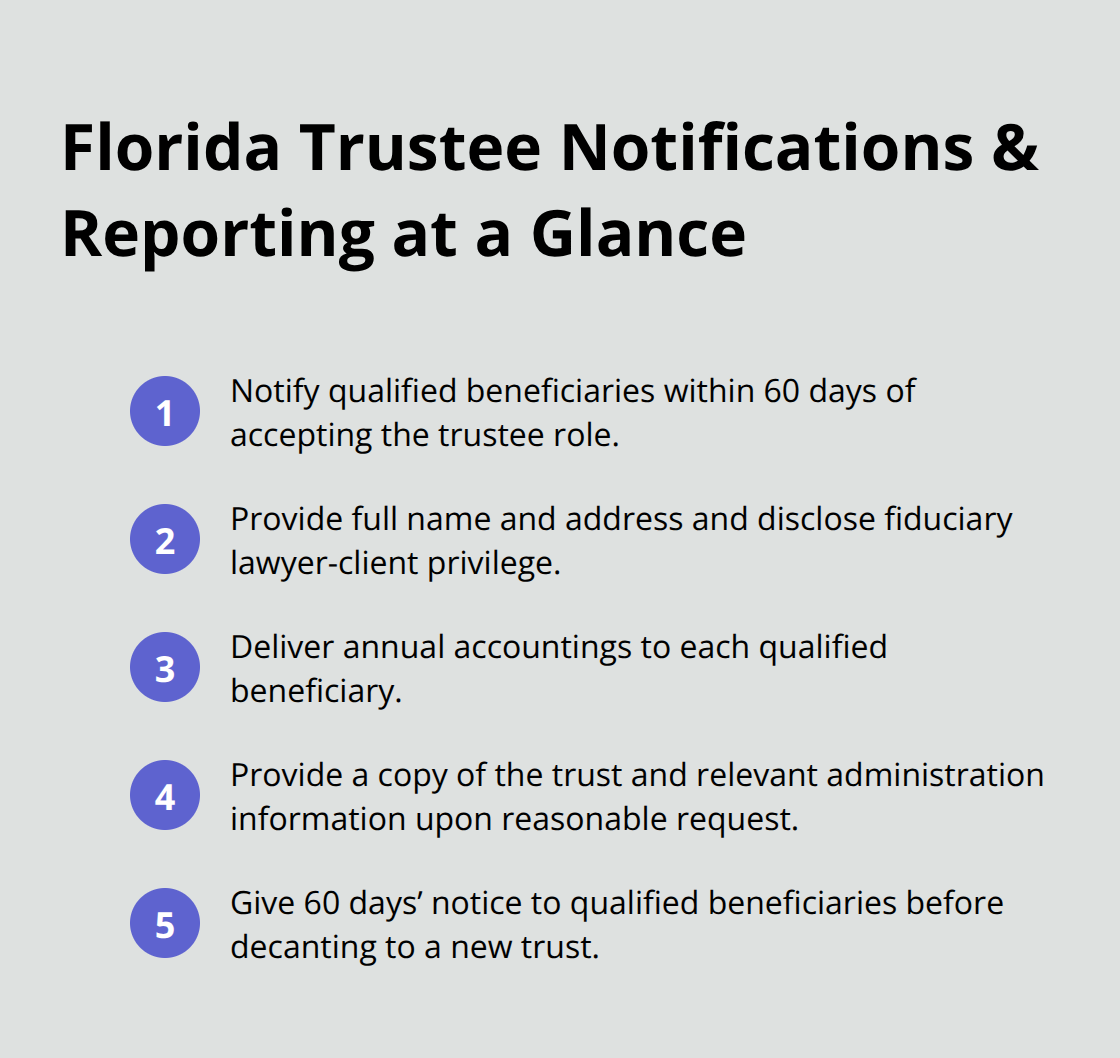

Florida Statutes Chapter 736, the Florida Trust Code, governs how irrevocable trusts operate. The law requires trustees to keep qualified beneficiaries reasonably informed about trust administration. Within sixty days of accepting the trustee role, the trustee must notify beneficiaries of acceptance, provide their full name and address, and disclose that fiduciary lawyer-client privilege applies. For irrevocable trusts, the trustee must provide annual accountings to each qualified beneficiary showing assets, liabilities, income, and distributions. Upon reasonable request, beneficiaries can demand a complete copy of the trust document and relevant information about administration.

The law also permits certain modifications. Uneconomic trusts with assets under approximately fifty thousand dollars can be terminated or modified through court order when administration costs exceed benefits. A trustee can also use decanting to create supplemental trusts with sixty days’ notice to qualified beneficiaries. Florida law does not allow self-settled irrevocable trusts to shield assets from the grantor’s own creditors if the grantor is also a beneficiary (a critical limitation). Homestead property presents special considerations. Florida’s constitution provides strong homestead protection, and transferring your home to an irrevocable trust can preserve those protections if you maintain a present possessory interest for life through specialized structures. The execution requirements are straightforward: sign with two witnesses and a notary, and include a self-proving affidavit to simplify future proceedings under Florida Statutes 736.0403.

Why Timing and Trustee Selection Matter

The decision to lock in your legacy through an irrevocable trust depends on when you want protection to begin and who you trust to manage your assets. Selecting the right trustee is essential because this person or entity will control your property for decades. A neutral third-party trustee often provides stronger asset protection than a family member, since creditors cannot easily pressure an independent fiduciary. The trustee’s duties include holding property, investing wisely, distributing income and principal according to the trust terms, handling taxes, maintaining records, and providing accountings to beneficiaries. Trustees are fiduciaries with a strict standard of care, meaning they must act in the beneficiaries’ best interests, not their own. Understanding these responsibilities helps you choose someone capable and willing to follow Florida law’s transparency requirements. The next section explores the specific situations where an irrevocable trust becomes the right choice for your family’s protection and wealth transfer goals.

When You Should Consider an Irrevocable Trust

An irrevocable trust becomes the right choice when you have assets worth protecting and you’re willing to permanently transfer ownership to gain that protection. The decision hinges on three practical scenarios that affect most families in Northeast Florida: shielding assets from creditors, reducing estate taxes, and planning for long-term care costs.

Asset Protection for High-Risk Professionals

Professionals in high-risk fields-doctors, contractors, business owners-benefit most from irrevocable trusts because they face genuine creditor exposure. Once assets move into an irrevocable trust, creditors cannot touch them, even if you face a lawsuit or judgment after the transfer. This protection works because the law treats the trust assets as belonging to the trustee, not to you personally. Revocable trusts offer zero creditor protection during your lifetime since they remain your property legally. The trade-off is permanent: you surrender control to gain security.

Estate Tax Reduction for Larger Estates

For estate tax purposes, irrevocable trusts remove assets from your taxable estate permanently. If your estate exceeds the federal exemption threshold (currently 13.61 million dollars per person in 2024), an irrevocable trust can save your heirs substantial money. Each dollar transferred to an irrevocable trust is one dollar that escapes estate tax at your death. For families with estates between 5 million and 13 million dollars, the tax savings alone justify the loss of control.

Medicaid Planning and Long-Term Care Protection

Medicaid planning demands irrevocable structures because Florida’s five-year look-back period requires assets to sit untouched in the trust for sixty months before you qualify for benefits. Waiting until you need long-term care is too late. Transferring assets now through an irrevocable trust protects them when nursing home or in-home care costs drain savings at 8,000 to 15,000 dollars monthly. The strategy only works if you plan ahead.

Specialized Irrevocable Trust Strategies

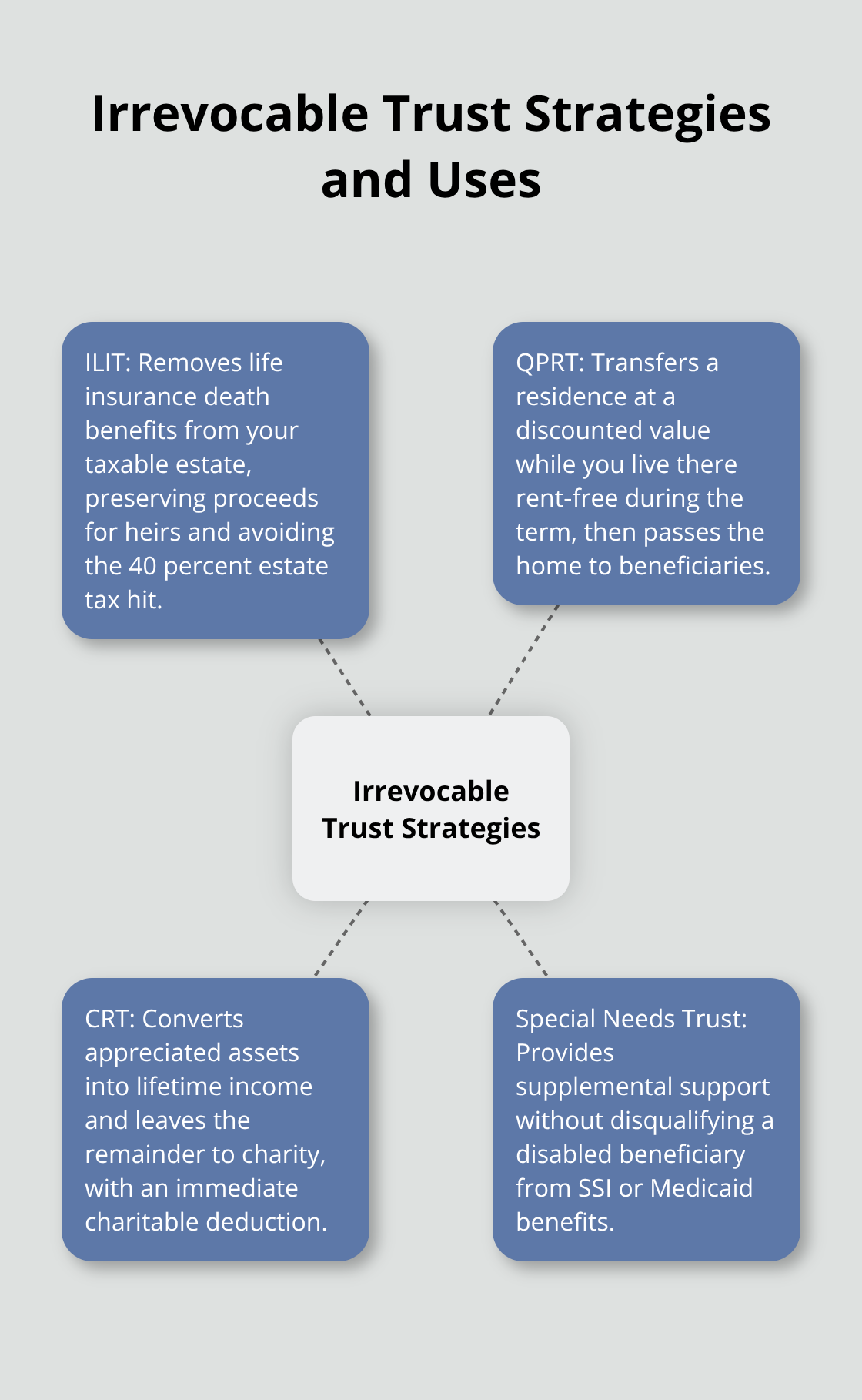

Irrevocable Life Insurance Trusts (ILITs) represent the most tax-efficient use of irrevocable structures for most families. Life insurance proceeds typically face estate tax, adding 40 percent or more to the tax bill your heirs owe. Placing a policy inside an ILIT removes the death benefit from your estate entirely, saving tens of thousands of dollars in taxes while keeping the cash available to your beneficiaries.

Charitable Remainder Trusts (CRTs) appeal to families who want to support causes they care about while generating lifetime income. You transfer appreciated assets into the trust, receive a fixed income stream for life or a term of years, and the remaining balance goes to charity. The upfront donation generates an immediate tax deduction that offsets capital gains from the appreciated assets.

Qualified Personal Residence Trusts (QPRTs) lock in the current value of your home for tax purposes while allowing you to live there rent-free for a set period. After the term ends, the home passes to your beneficiaries at a discounted value, reducing gift taxes.

Special Needs Trusts protect disabled family members by allowing ongoing support without disqualifying them from SSI or Medicaid benefits. These trusts require careful drafting to comply with federal rules, but the payoff is enormous-your loved one receives care without losing essential government assistance.

Selecting the Right Trustee for Maximum Protection

The trustee’s choice matters more in irrevocable structures than in revocable ones. A neutral third-party trustee provides stronger creditor protection and complies with Florida law’s strict notification and accounting requirements. Family members often lack the distance needed to resist pressure from creditors or other beneficiaries. Your attorney can help you evaluate trustee options before you commit to an irrevocable structure, since the choice affects protection levels and family dynamics for decades. Once you understand which irrevocable strategy fits your goals, the next step involves understanding how trust structures work under Florida law and what obligations your trustee must fulfill.

Which Irrevocable Trust Strategy Fits Your Goals

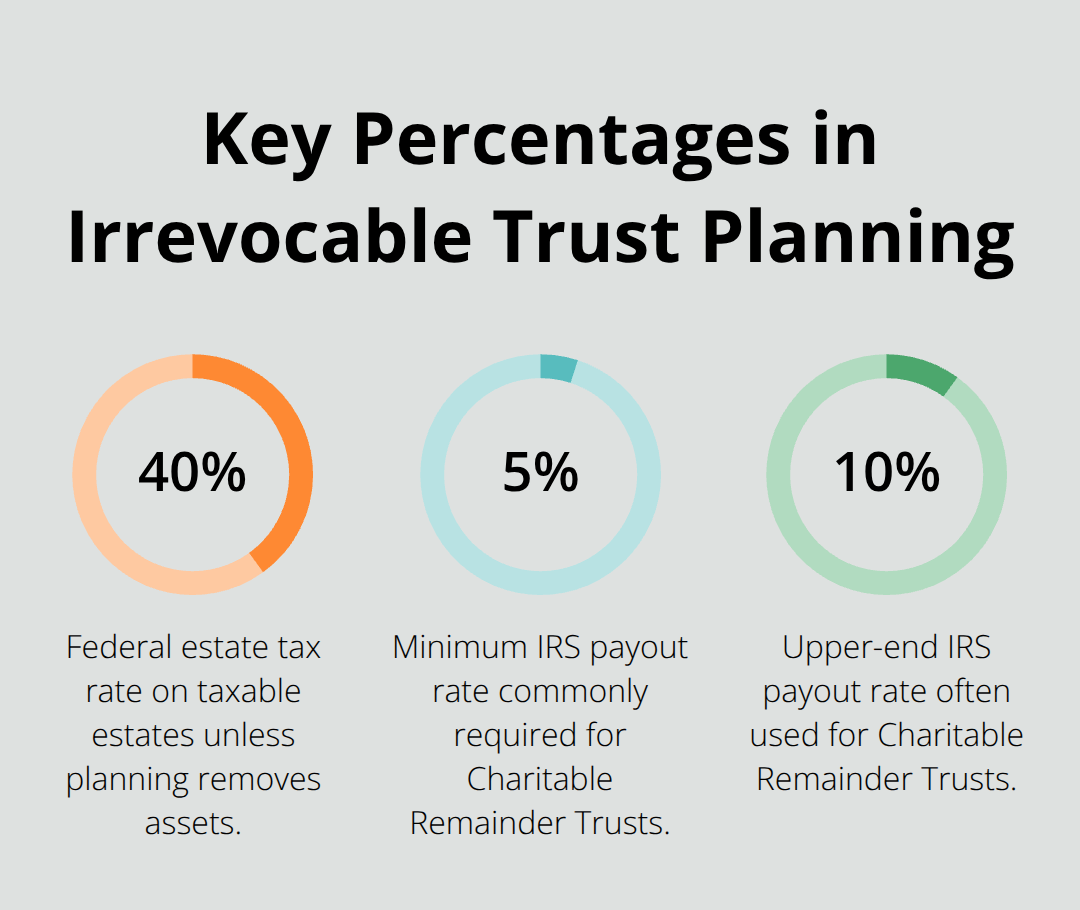

Life insurance trusts, residence trusts, and charitable trusts each solve different wealth transfer problems. The right choice depends on your assets, family situation, and tax bracket. An Irrevocable Life Insurance Trust (ILIT) works best if you own a substantial life insurance policy. The federal estate tax rate sits at 40 percent, meaning a two million dollar death benefit costs your heirs eight hundred thousand dollars in taxes unless the policy sits outside your taxable estate. Moving the policy into an ILIT removes it entirely, keeping the full benefit available to your family.

How ILITs Protect Your Death Benefit

The mechanics require careful timing: you cannot transfer an existing policy into an ILIT and expect full protection if you die within three years of the transfer, since the proceeds still face estate tax under the three-year rule. However, if you create the ILIT first and have the trustee purchase a new policy, the death benefit escapes taxation completely. For families with policies worth five hundred thousand dollars or more, this strategy saves hundreds of thousands in taxes. The trustee must comply with strict rules: annual notices to beneficiaries about their rights to withdraw contributions, called Crummey letters, are mandatory under federal law or the tax benefits disappear.

QPRTs and Discounted Home Transfers

A Qualified Personal Residence Trust (QPRT) locks in your home’s current value for gift tax purposes while you live there rent-free during the trust term. If your home is worth one million dollars today and you establish a ten-year QPRT, the gift tax value drops significantly because the IRS discounts the value based on your retained right to occupy the property. After ten years, the home passes to your beneficiaries at that discounted value, saving gift and estate taxes. The downside is clear: after the term ends, you must pay fair market rent to stay in your home or move out. This strategy makes sense only if you plan to downsize eventually or if your family is willing to charge you rent that satisfies IRS standards.

Charitable Remainder Trusts for Income and Legacy

Charitable Remainder Trusts (CRTs) appeal to families with appreciated assets they want to convert into lifetime income while supporting charitable causes. You transfer appreciated real estate or securities into the trust, receive a fixed income stream for life or twenty years (whichever you choose), and the remaining balance goes to qualified charities. The strategy produces an immediate charitable deduction that offsets capital gains taxes from the appreciated assets. If you own real estate worth two million dollars with a one million dollar gain, transferring it into a CRT eliminates the capital gains tax, provides lifetime income, and delivers a substantial charitable deduction. The IRS requires specific payout rates: between five and ten percent annually depending on your age and trust type. A seventy-year-old typically receives higher payouts than a fifty-year-old in the same CRT structure.

Special Needs Trusts for Disabled Beneficiaries

Special Needs Trusts solve a completely different problem: protecting disabled beneficiaries without disqualifying them from SSI or Medicaid. These trusts allow the trustee to pay for expenses SSI does not cover-education, therapy, recreation, personal care items-while the government continues providing health coverage and basic income. The trust must be drafted precisely to avoid language that triggers disqualification. Supplemental needs language, which emphasizes paying for items the government does not cover rather than basic support, is essential. Without this careful drafting, a five thousand dollar distribution for therapy equipment could disqualify your loved one from thousands in annual benefits.

Execution and Trustee Compliance Matter

The three-year rule for life insurance, the discount calculations for residence trusts, and the payout requirements for charitable trusts all demand precise execution. Tax planning with a trust is more flexible than with a will, and an irrevocable trust can remove assets from your taxable estate and reduce or eliminate federal taxes. Trustees managing these structures must understand their obligations under Florida law, including annual accountings to beneficiaries and timely notice of acceptance within sixty days. Each strategy also carries different trustee duties and beneficiary notification requirements. The complexity is why experienced estate planning attorneys recommend working with qualified professionals before committing to any irrevocable structure-the wrong choice or improper execution costs your family money for decades.

Final Thoughts

Locking in your legacy through an irrevocable trust in Florida requires you to weigh permanent protection against the loss of control. Creditor protection, estate tax reduction, and Medicaid planning represent the three core reasons families commit to these structures, and each applies to different situations depending on your assets, profession, and long-term care concerns. The right strategy-whether an Irrevocable Life Insurance Trust, Qualified Personal Residence Trust, Charitable Remainder Trust, or Special Needs Trust-solves a specific problem, but all demand precise execution and trustee compliance with Florida law’s notification and accounting requirements.

We at Family, Estate & Mediation Law help clients across St. Augustine and Palatka evaluate whether an irrevocable trust in Florida fits your family’s goals and which structure protects your assets most effectively. Our team works with you to select the right trustee, structure the trust properly, and fund it completely so your protection actually works when it matters most. Whether you own substantial life insurance, face creditor exposure in your profession, or want to plan ahead for long-term care, we can help you determine the best path forward.

Contact us to discuss your specific situation and schedule a consultation with our team in St. Augustine or Palatka. Visit Family, Estate & Mediation Law to take the next step toward protecting your family’s future.