A trust is one of the most powerful tools you can use to protect your family’s wealth and control what happens to your assets after you’re gone. At Family, Estate & Mediation Law, we’ve helped countless families understand that trusts creation steps don’t have to be complicated or overwhelming.

The right trust structure can save your heirs thousands in taxes, keep your assets out of probate court, and give you peace of mind knowing your wishes will be followed exactly as you intended. This guide walks you through everything you need to know.

Why Your Family Needs a Trust

Probate costs your family time and money

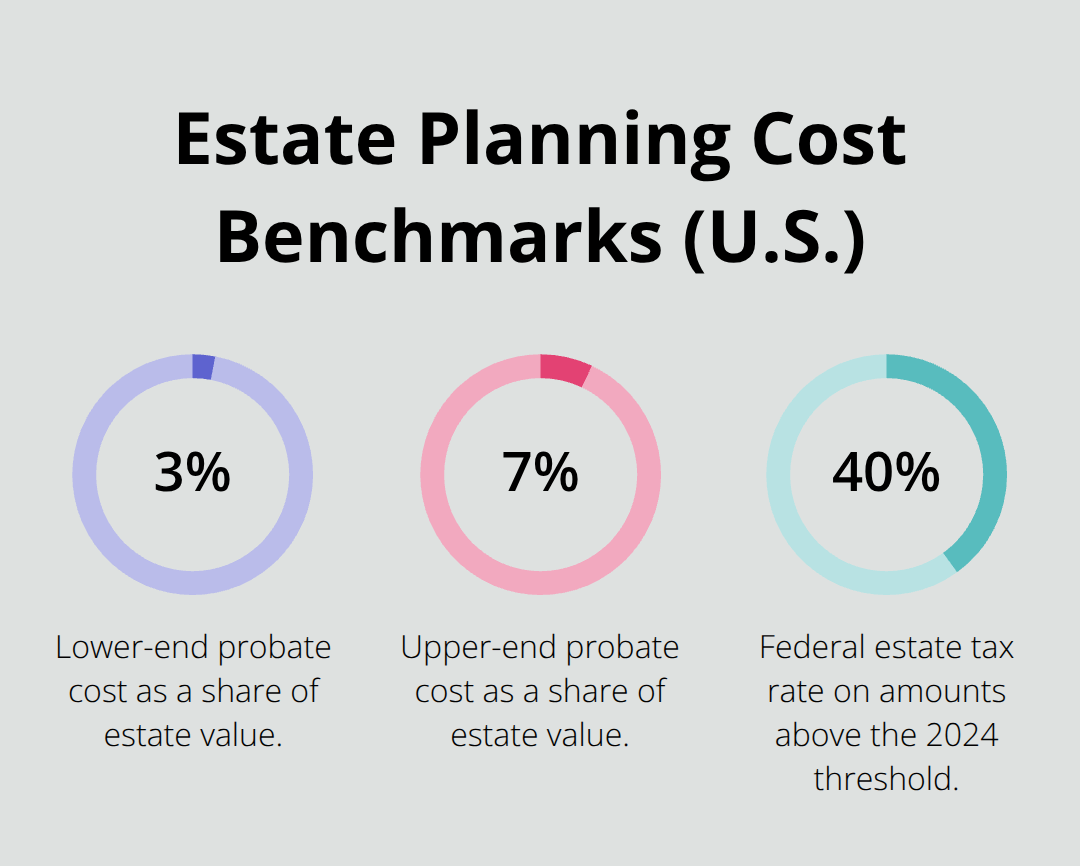

Probate court is expensive, slow, and public. When you die without a trust, your estate enters probate where a judge oversees asset distribution, creditors file claims, and your family details become court records anyone can access. The American Bar Association reports that the average probate case costs between 3% and 7% of your estate’s value and takes 8 to 12 months to complete.

A trust bypasses probate entirely. Your assets transfer directly to your beneficiaries outside the court system, keeping your financial information private and getting money to your family months faster than a will ever could.

You control when beneficiaries receive their inheritance

Without a trust, your beneficiaries receive their inheritance as a lump sum once probate closes. A trust lets you set conditions on when and how they receive money. You can delay distributions until a child reaches 30, require a beneficiary to finish college before receiving funds, or spread payments over decades. This approach protects young heirs from making poor financial decisions with sudden wealth and prevents a spendthrift relative from depleting their inheritance in months. You also maintain control if circumstances change-an irrevocable trust created during your lifetime removes assets from your taxable estate and shields them from creditors, while a revocable living trust lets you modify terms or reclaim assets if needed.

Estate taxes take a massive bite from family wealth

Federal estate taxes hit estates over $13.61 million in 2024, taking 40% of assets above that threshold. State taxes apply at lower thresholds in many jurisdictions. An irrevocable trust structured properly removes assets from your taxable estate, reducing or eliminating estate taxes your heirs would otherwise owe. A married couple using trust strategies can shelter double that amount. This tax savings compounds across generations. If your family business or real estate portfolio appreciates significantly, a trust prevents your heirs from inheriting a massive tax bill that forces them to sell assets to pay taxes (something that happens far too often in family transitions). The difference between proper trust planning and no planning can mean hundreds of thousands of dollars staying in your family instead of going to the government.

Now that you understand why a trust matters, the next step involves making concrete decisions about what you actually want to accomplish with your trust structure.

Building Your Trust From the Ground Up

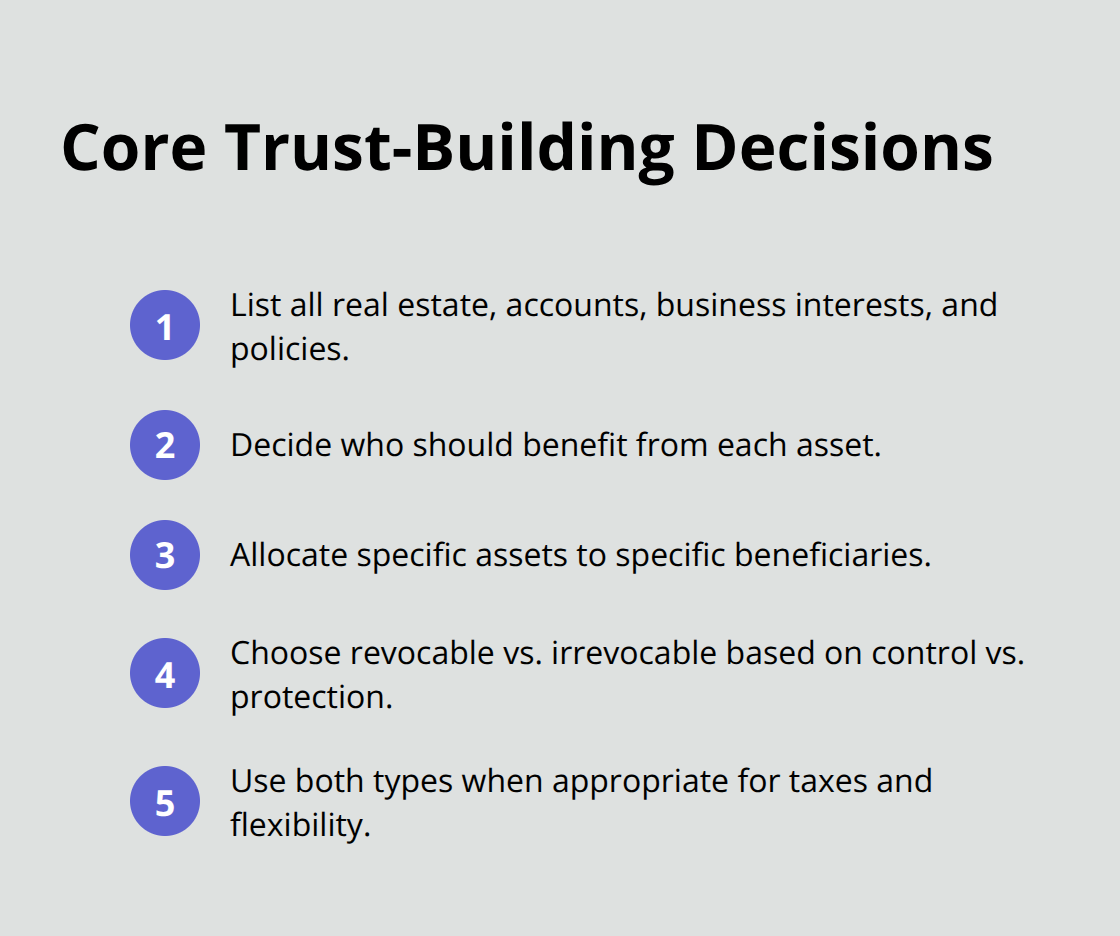

Start by listing every asset that matters: real estate, investment accounts, business interests, life insurance policies, and personal property with significant value. Most people underestimate what they own until they sit down and inventory it. Once you know what you have, identify who should benefit. This sounds straightforward, but it’s where family dynamics become real.

You might want your primary residence to go to your spouse, business assets to your oldest child who runs the company, and liquid investments distributed equally among all three children. A trust lets you split assets this way instead of forcing an all-or-nothing distribution. Next, decide between a revocable living trust and an irrevocable trust. A revocable living trust gives you maximum flexibility during your lifetime-you can modify beneficiaries, add or remove assets, or reclaim everything if circumstances change. This works well if your situation might shift or you want to maintain control. An irrevocable trust locks in your decisions but removes assets from your taxable estate permanently, which cuts estate taxes significantly and shields those assets from creditors. Many families use both: a revocable trust for day-to-day control and an irrevocable trust for specific assets like life insurance or real estate that benefit from tax protection. The choice depends entirely on whether you value flexibility more or tax savings and creditor protection.

Your trustee makes or breaks execution

Your trustee manages trust assets, pays bills, files taxes, and distributes money to beneficiaries according to your wishes. This person carries serious legal responsibility. You might name yourself as trustee while alive, then designate a successor trustee to take over after you die. Many people name a spouse, adult child, or trusted friend. The problem: that person may lack financial skills, become overwhelmed with accounting requirements, or face family conflict when making distribution decisions. Professional trustees-banks, trust companies, or individual fiduciaries-charge fees (typically 0.5% to 1% of assets annually) but handle all the paperwork, file required accountings, manage investments, and stay neutral when beneficiary disputes arise. For smaller estates under $500,000, a capable family member often works fine. For larger estates or complex situations (like blended families or a special needs child), a professional trustee prevents costly mistakes and family resentment. Work with an attorney to draft documents that clearly define what your trustee can and cannot do, which reduces ambiguity and protects them from liability.

Documents done right the first time save thousands later

This is where you need an attorney-not a DIY online service. Your state’s trust laws are specific. Florida trusts, for example, have different rules than California trusts regarding trustee powers and beneficiary notification requirements. An attorney drafts language tailored to your situation, identifies tax implications, coordinates your trust with your will, and makes sure asset titles transfer properly. They’ll also spot issues you’d miss: if you name a minor as trustee, if your irrevocable trust language conflicts with your tax goals, or if your chosen trustee lacks authority to manage business assets. The cost typically runs $1,500 to $5,000 for a straightforward trust, far less than litigation that results from poorly drafted documents. Once the attorney finalizes everything, you must fund the trust by transferring assets into it. This is the step people skip, which renders the entire trust useless. Retitle your house deed, change investment account registrations, and update beneficiary designations on life insurance and retirement accounts. Your attorney should provide a funding checklist so nothing gets missed.

With your trust structure in place and documents finalized, the real work begins-moving assets into the trust and establishing the systems that keep it functioning smoothly for years to come.

Managing Your Trust After Creation

Transfer assets into your trust immediately

Funding your trust separates a document that protects your family from an expensive piece of paper that does nothing. You must retitle assets into the trust’s name for it to control them. Start with your primary residence by contacting your county clerk’s office and filing a new deed that transfers ownership from your name to your trust name. This typically costs $50 to $200 and takes a few weeks. For investment accounts, call your bank or brokerage and request a change of registration form, providing your trust document and new account registration details. Life insurance policies require a beneficiary designation change-most carriers process this within days. Retirement accounts like IRAs and 401(k)s have special rules; consult a tax advisor before transferring these because moving them into a trust can trigger unexpected tax consequences. Real estate owned in multiple states needs separate deeds in each jurisdiction following that state’s recording requirements.

Create a checklist with your attorney of every asset that should transfer, then work through each one methodically. Track which accounts you’ve already updated so nothing gets overlooked. A common mistake occurs when people retitle everything, then purchase new property or open new investment accounts without adding them to the trust. Your trust only controls what’s inside it, so any assets acquired after funding must be added manually or they’ll bypass the trust entirely.

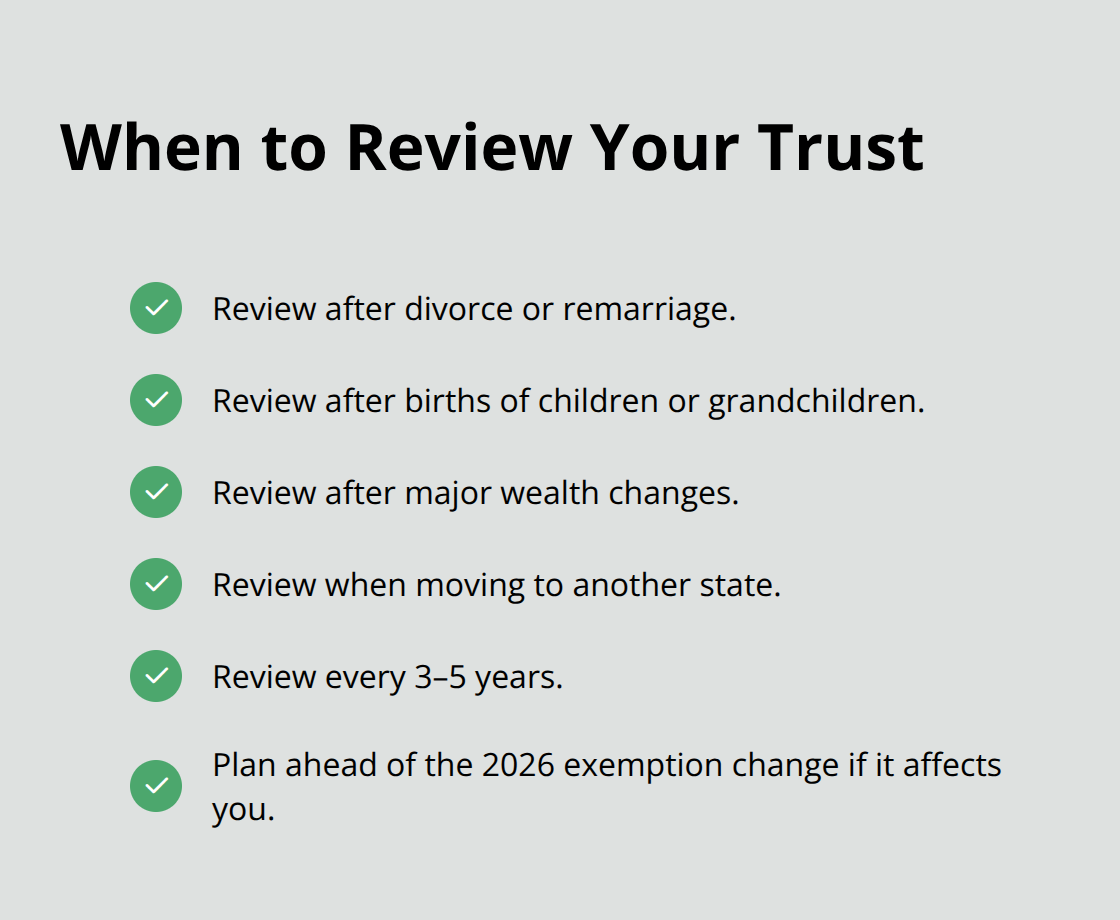

Review your trust as circumstances shift

Your trust isn’t static-it needs periodic reviews as your life changes and tax laws shift. Major events like divorce, remarriage, the birth of children or grandchildren, significant wealth changes, or moving to a different state should trigger a trust review with an attorney. Even without major changes, review your trust every three to five years because tax laws change frequently. The federal estate tax exemption was $13.61 million per person in 2024, but it’s scheduled to drop to approximately $7 million in 2026 unless Congress acts. This deadline makes 2025 and early 2026 critical planning windows for families with substantial assets.

Communicate trust details with your trustee and beneficiaries

Your trustee and beneficiaries need to understand the trust’s terms and their roles before you die or become incapacitated. Schedule a family meeting where you explain the trust’s purpose, name your trustee, and discuss how distributions will work. Many families avoid this conversation because it feels uncomfortable, but beneficiaries who understand your reasoning ahead of time are far less likely to dispute the trust or blame the trustee later. Provide your trustee with a written summary of their duties, contact information for your attorney, and location of important documents.

Store documents securely and provide copies

Store the original trust document in a safe deposit box or fireproof safe at home, and give your trustee a certified copy. If your trustee is a professional fiduciary or bank, they’ll handle ongoing communication with beneficiaries and provide annual accountings showing all trust income, expenses, and distributions. If you’ve named a family member as trustee, they must understand they’re legally required to provide beneficiaries with copies of trust documents and detailed accountings upon request. Trustees who fail to communicate or provide accounting information face lawsuits from beneficiaries seeking removal and damages. The trustee’s job becomes easier when expectations are crystal clear from the start.

Final Thoughts

Creating a trust transforms your estate plan from a generic document into a personalized strategy that protects what matters most. The trusts creation steps we’ve outlined-identifying your assets, choosing the right trust type, drafting proper documents, funding everything correctly, and maintaining your plan over time-work together to accomplish what a will simply cannot. Your family avoids probate delays and costs, your beneficiaries receive distributions on your timeline, and your heirs sidestep massive estate tax bills that would otherwise drain your legacy.

This process requires more than good intentions. It demands clear thinking about your goals, honest conversations with family members, and professional guidance from someone who understands both the legal requirements and your personal situation. At Family, Estate & Mediation Law, we’ve worked with families across Northeast Florida, helping them build trusts that actually work when they’re needed most.

The best time to act is now, not when a health crisis forces rushed decisions or when your family faces conflict over your wishes. Start by gathering your asset list and identifying your beneficiaries, then contact an attorney who can review your specific situation and draft documents tailored to your goals.